Accrued revenue is a type of revenue that companies earn upon delivering or performing a good or service but has not yet invoiced the customer or client.

On a balance sheet, accrued revenue represents the money owed to a business and thus is an asset.

It is a form of revenue that is very common among service-related businesses, which often utilize an accrual accounting method to track and balance accrued revenue, as well as accrued expenses, in order to ensure their financial statements are accurate for every accounting period.

On a balance sheet, companies can consider accrued revenue an asset, as it is a resource with financial value that the company owns or controls, with the understanding that it will provide benefits for it in the future.

In some cases, accrued revenue may specifically be classified as a "current asset" on a balance sheet if the payment it represents is expected to be billed within a single year.

However, if it is planned to take more than a year for the invoice to be sent, it would then be labeled as a "long-term asset" or "other asset."

Once a company officially bills for the goods or service, the accrued revenue account will decrease while the accounts receivable account will increase, indicating that the amount owed has been billed and now the company is awaiting payment.

Accrued revenue is a vital element of our financial system, allowing businesses and customers to perform a diverse variety of transactions and contracts beyond straightforward cash payments.

Why is accrued revenue so crucial for businesses?

Accrued revenue serves a very important role for businesses, especially those that employ an accrual accounting method — a form of accounting that recognizes the occurrence of a transaction even if it hasn’t been billed yet.

Here are some reasons why accrued revenue is so significant in business today:

Accurate financial statements

For businesses with long term contracts, accrued revenue allows them to record revenue that has been earned during the accounting period instead of when it is finally billed to a customer.

Some contracts might require billing after the project is 100% completed instead of as the work is being done.

This ensures financial statements more closely reflect a company's financial position and activity to investors, creditors, and managers, allowing them to make well-informed decisions.

Compliance & fulfillment

On the one hand, a company recognizing accrued revenue on their financial statements may have tax implications, depending on the laws and tax jurisdiction of where their business resides.

In addition, a business in an industry that involves long-term projects and contracts, such as a construction company, can utilize accrued revenue to track the progress of contract fulfillment as well as compliance with industry regulations.

Helpful performance indicator

Accrued revenue can benefit businesses by offering valuable insights into how well certain aspects of a company are performing.

For example, a high accrued revenue on the books may indicate that a particular business also has a large number of longer term contracts. This would mean without accrued revenue the revenue and profits of a business would appear lumpy and give not give useful information on how a business is performing.

Furthermore, when companies recognize accrued revenue, they help maintain confidence among their stakeholders, resulting in them providing dependable and transparent financial reports.

Through the principles of accrual accounting, accrued revenue has helped numerous businesses across a wide variety of industries keep track of their projects and ensure they receive every dollar they deserve, regardless of whether they are paid at the end of a transaction or later on.

Learn how BILL can help ensure smooth, unimpeded cash flow through our easy-to-manage AP/AR platform and its streamlined invoicing features. Boost your business's financial prowess with BILL today!

Accrued revenue & accrual accounting

Since accrued revenue is a product of it, it is important to understand what accrual accounting is in order to better comprehend the roles and purpose of accrued revenue. Below, we define accrual accounting, as well as some of its principles in relation to accrued revenue:

What is accrual accounting?

There are two primary accounting methods. One is cash accounting, which only attributes a company's revenue to cash transactions that they receive directly from their client or customer. The other method is accrual accounting, which takes into account when the revenue is earned and when an expense is incurred regardless of cash being received or spent.

Accrual accounting is a more common method of accounting today because it provides a more accurate measure of a company's financial position and operational success.

The central principle is that both revenue and expenses should be recognized in a company's financial statement, whether or not they have been received or paid. Revenue should be recognized once it is earned while expenses are recognized as they are incurred.

This ensures that every transaction is precisely accounted for in its appropriate accounting periods, thus providing an accurate representation of a company's operations.

3 Important principles of accrual accounting

Several different principles underpin the methods of accrual accounting, ensuring companies using them stay consistent with their best practices.

Doing so allows companies to continuously achieve their desired outcomes while also maintaining a stable cash flow between businesses. Here are three crucial principles:

Revenue recognition principle

Among the most foundational principles of accrual accounting is the revenue recognition principle. This principle indicates that a business should record the revenue at the time that it earned, not necessarily when the cash is received.

In addition, the revenue recognition principle has its opposite — the expense recognition principle, where a company must also record when they produce an expense, but not necessarily when the expense has been paid.

These principles thus require the existence of both accrued revenue and accrued expense, as both allow accountants to record their company's earnings and expenses while indicating they have yet to make or receive payment.

Businesses that take care to follow proper revenue recognition principles will more than likely keep track of their accrued revenue consistently through each given accounting period.

Matching principle

In addition to the principle of revenue recognition, another fundamental principle of accrual accounting is the matching principle.

The matching principle emphasizes that companies should record accrued revenues as well as accrued expenses, all within the same accounting period.

This practice ensures that accountants, as well as executives, investors, and other stakeholders, all hold a clearer picture of a company's financial position from one period to another.

Conservatism principle

Finally, the conservatism principle is among several generally accepted accounting principles in accrual accounting.

This principle promotes a cautious approach, encouraging accountants to only record accrued revenues and other gains when they are reasonably certain they will be received.

In addition to that, the conservatism principle also dictates that companies should also record expenses and other losses when they are considered probable.

In essence, the conservatism principle seeks to ensure businesses retain a focused and grounded perspective of their financial outlook in order to make better decisions.

Along with several more, these principles ensure companies that use accrual accounting maintain a clear and accurate view of their business's financial health.

Utilize BILL's Account Receivable and Accounts Payable controls for better decision-making and streamlined tracking of approvals and invoice payments.

What is an adjusting journal entry?

In accrual accounting, an adjusting journal entry is where a company's financial activity is recorded, specifically activities that have not yet been placed on a company's general ledger but must be accounted for before the end of an accounting period.

A well-kept adjusting journal entry ensures financial statements are complete and accurate from one period to the next. An adjusting entry will often be made at the end of a company's given period, whether it is monthly, quarterly, or annually.

Typically, there are five main types of adjusting entries that a company will record, including:

- Accrued Revenues

- Deferred Revenue (also called "unearned revenue")

- Accrued Expenses

- Prepaid Expenses

- Depreciation

These adjusting journal entries ensure that a company's balance sheet and other financial statements are prepared in accordance with the best practices of accrual accounting and accurately reflect its financial position and performance for a specific period.

Accrued revenue vs. different types of revenue

As indicated previously, the accrual accounting process will allow a company to have more than one form of revenue on its balance sheet.

To understand the nuances of accrued revenue, let's compare it with these other forms of revenue:

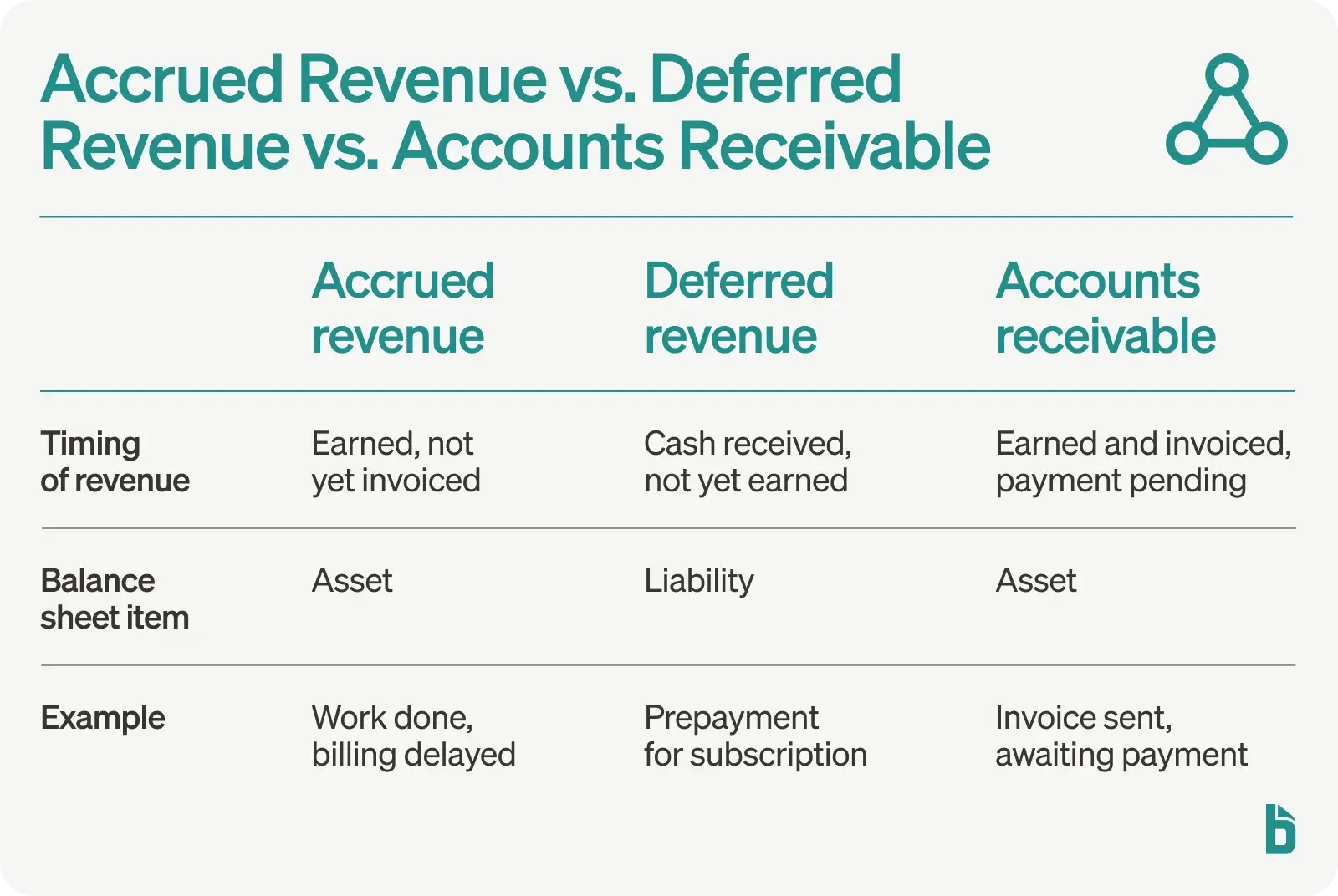

Accrued revenue vs. deferred revenue

Accrued revenue is income that has been earned but not recorded in a company's books because an invoice has yet to be sent to the customer or client.

On the other hand, deferred revenue involves payments received before a company delivers its goods or services.

For both types of revenue, an adjusting entry will be made before the end of an accounting period to ensure they are recognized.

The main difference is that accrued revenue is earned now but will be billed later, while deferred revenue the payment is received the goods or services have been delivered.

Accrued revenue vs. accounts receivable

Accrued revenue and accounts receivable are both closely related but still refer to two different occurrences within a transaction between a company and its customers.

First, accrued revenue indicates that revenue has been earned but the company has not yet billed the customer for the goods or services.

Accounts receivable signifies when a company has earned the revenue and billed the customer for the goods or services. The company is now awaiting payment from the customer.

Example of accrued revenue

Finally, let's further clarify how accrued revenue appears on a company's adjusting journal entry, as well as some real-world examples of accrued revenue that individuals and businesses often interact with:

There are a number of businesses that must utilize an accrual accounting method to operate effectively and thus produce accrued revenue through their accounting periods.

Here is an examples of accrued revenue one may find.

Long-term projects

There are numerous businesses that work on long-term projects for their clients and thus require a form of accrued revenue.

Some contracts could indicate that billing happens once the project is completed. The company will want to accrue revenue on a percentage of completion method to show movement as well as financial performance to their stakeholders.

A strong example would be a construction company building a large-scale commercial property over the course of a year, earning accrued revenue as work is completed but still needs to be billed.

Track & record accrued revenue with BILL

Accrued revenue is one of the numerous pieces of financial information that a business must keep track of to maintain an accurate perspective of its financial health.

Streamline accounting workflows and preserve your company's financial health with BILL's intuitive accounts receivable and accounts payable system.

For large and small businesses, we provide a powerful AP/AR with many robust features that can help achieve greater efficiency and satisfaction for customers, vendors, and staff members.

Find out how BILL can transform your business's accounts receivable processes today.