Bank transit numbers, also known as routing numbers, provide unique identifiers for banks and other financial institutions and ensure secure funds transfers across a variety of channels, including physical checks, wire transfers, and online banking transactions.

Bank transit numbers may not sound familiar, as they go by other names among different banks from one country to another.

This can make the term seem challenging to understand, but it is simple to grasp once explained.

In this article, we will discuss:

- What is a bank transfer number

- How bank transit numbers are important

- The parts of a bank transit number and what they indicate

- How bank transit numbers differ from other essential numbers

- Bank transit number vs routing number

Bank transit number definition

A bank transit number is commonly referred to in the United States as a routing number. It is a nine-digit number that is associated with a particular bank or other financial institution.

Every financial institution has a specific bank transit number tied to them, which means that each person who holds an account with them will share the same bank transit number.

Bank transit numbers are one number among many that will exist on a physical or digital financial instrument — essentially a financial document that indicates payment of a certain amount of money, such as a paper check or promissory note.

How bank transit numbers help financial institutions

In 1910, the American Bankers Association (ABA) developed the system behind bank transit numbers in order to provide an organized and secure method of delivering paper checks from one bank to another so account holders could receive funds in their accounts.

Today, both small and big banks, as well as other financial institutions, require the use of bank transit numbers. They function as a vital piece of information in crucial financial transactions, including:

- ACH Payments

- Wire payments

- Bill payments

- Checks

- Direct deposits

Bank transit numbers continue to facilitate transferring money from one bank or financial institution to another, even through electronic transactions such as your bank's mobile app.

Here are some other examples of how bank transit numbers are used:

- The US Federal Reserve Bank uses bank transit numbers through their Fedwire funds transfer system when processing checks and other forms of payment into bank accounts.

- The automated clearing house (ACH) Network utilizes bank transit numbers to process direct deposit payments, bill payments, and other types of electronic money transfers.

Bank transit numbers have a highly-influential history in the development and current state of our modern-day financial institutions.

It is also a vital piece of information for every business to save in order to identify where the business holds their banking accounts and financial instruments.

Parts of a bank transit number

You can find your bank transit number at the bottom left corner of a check that you receive from your checking accounts, as well as through your online banking account or on your bank statement.

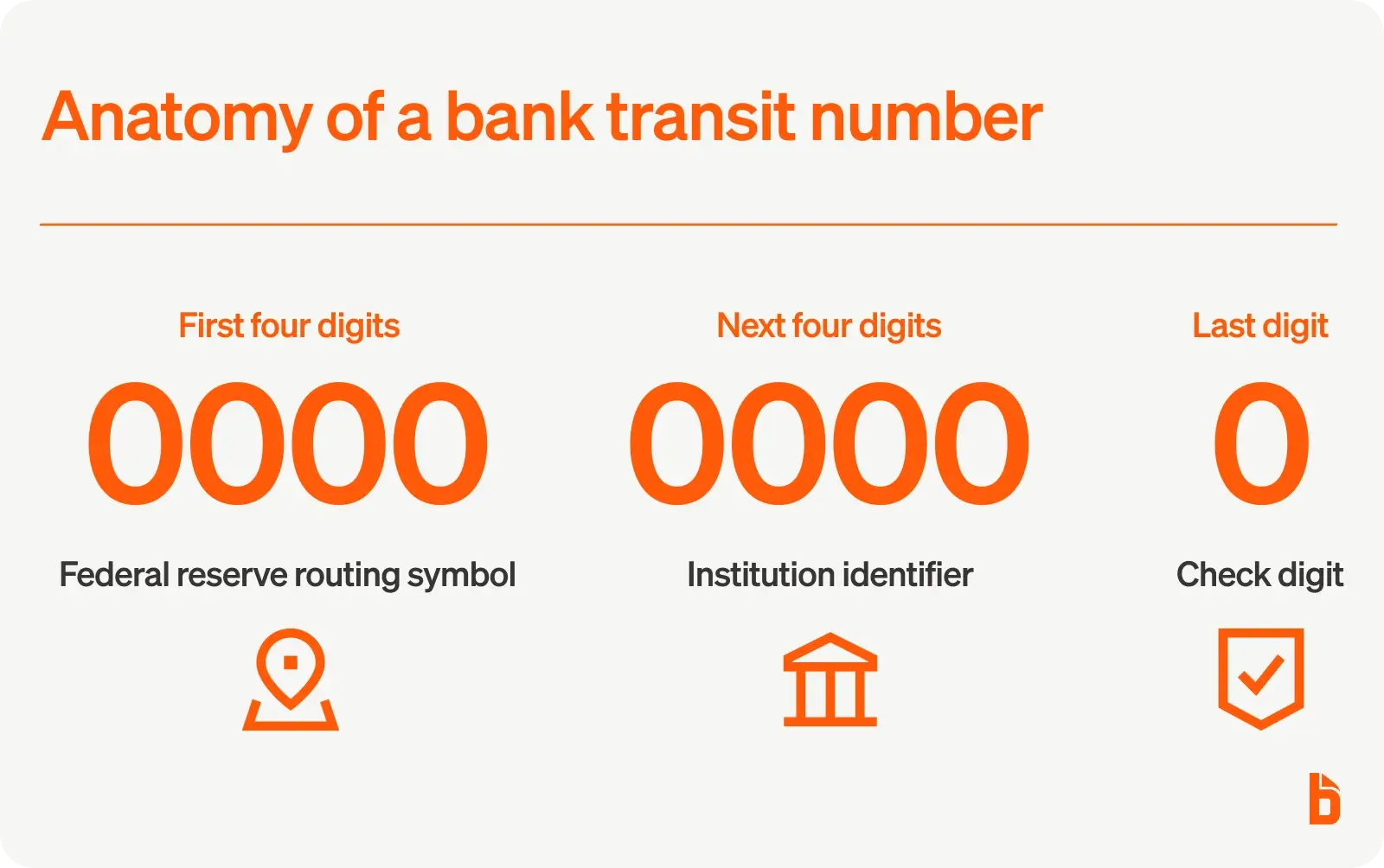

In the United States, bank transit numbers are a nine-digit number sequence. Other countries will have different lengths and formats depending on the banks' country of origin.

The nine digit code can be split into three sets, each indicating more information on the bank or financial institution responsible for the money in a given financial transaction.

Here are the three parts of a bank transit number:

The first four digits

Specifically in the US, the first four of a bank transit number's nine digits are the Federal Reserve Routing Symbol. They indicate which Federal Reserve District the bank of origin is in.

The second four digits

The next four digits in the sequence identify the specific bank or financial institution from which the money is being transferred.

The last digit

The final number is a check digit, which is used by sorting machines to check if there is an error or redundancy when sorting through many bank transit numbers across numerous checks.

This also ensures that all financial transactions, whether paper check deposits or an electronic wire transfer are authentic and secure.

With multi-layered security weaved into its payment processing platform, BILL ensures all online business transactions are safe and secure for you and your vendors.

How a bank transit number is different

The bank transit number differs greatly in purpose among the many identification numbers associated with financial accounts. Here are a few comparisons between a bank transit number and other financial identification codes.

Bank transit number vs bank account number

The key difference between a bank account number and a bank transit number is that one is associated with one's specific account within a bank or other financial establishment (account number), while the other identifies that specific bank the account holder has an account at (transit number).

Bank transit number vs routing number

This comparison requires some explanation, as the bank transit numbers are synonymous with bank routing numbers in the US. Both serve the same purpose and carry the same definition. However, this differs in other banks in various countries.

For example, in Canada, the transit number is a five-digit code that also identifies the specific bank branch a person holds an account at, or more simply, it is the bank's address number. It is then combined with the bank's institution numbers to form a complete bank routing number.

In this case, both US and Canadian bank transit numbers serve the same purpose but differ in their formats and meaning. Moreover, banking systems in other countries may differ in routing number formats as well.

Simplify pay across financial institutions with BILL

Understanding what a bank transit number is can aid in navigating the complexities of the financial world. However, to simplify cash flow for your business, you'll need the right tools in place.

Connect BILL's automated AP and AR platform to your business's bank account, and you'll be able to make and receive payments through ACH, credit card, international wire transfers, and more.

Simply add in the proper account information, including bank transit numbers, and enjoy focusing on your business with all your financials taken care of.

Reach out and learn more about how BILL's intuitive AP/AR and invoice automation will benefit your business today!