Do you know how much sales revenue a business would need to break even?

The break-even point is one of the most informative metrics in the accountant’s toolkit. It can help determine what selling price will be profitable to use and how far sales can decrease before a business starts losing money.

It’s also relatively easy to calculate. Knowing a company’s fixed costs and contribution margin will allow them to determine their break-even point.

Then, after analyzing it, you can draw out several insights that can drive smarter decision making processes and business success. Let’s take a look at what the break-even point is and why it matters.

In this article, you’ll learn:

- What the break-even point is

- Why the break-even point matters

- How to calculate the break-even point

- How to do a break-even analysis

What is the break-even point?

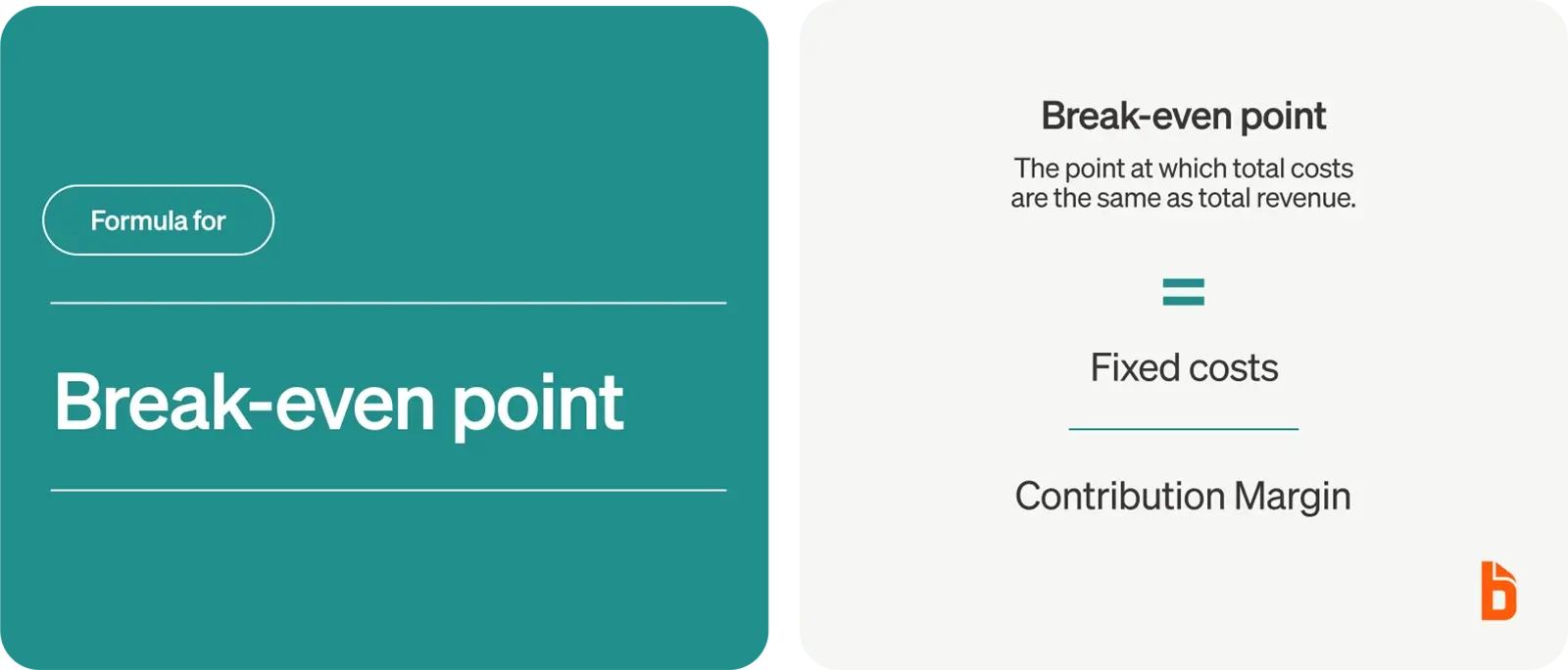

The break-even point is the point at which total costs are the same as total revenue.

In other words, a business’s break-even point is the sales revenue needed to break even. Selling a higher number of units or having a higher turnover than the break-even point means a company turned a profit. On the other hand, selling less than the break-even point means they are taking on losses.

Knowing the break-even point also helps in other areas, from budgeting to smarter financial decision-making. Here are some benefits for understanding when a business breaks even:

Make more rational financial decisions

Should a business invest in a new machine or launch a new product line? Moving ahead with a new project, product, or investment might seem like a good idea. After all, it’s going to bring in more revenue.

But if you don’t know the relationship between total costs and the total expected revenue, you won't know if it’s truly a good idea. The break-even point shows companies how much they’ll need to earn in revenue in order to break even, enabling them to make decisions based on the numbers rather than on intuition.

Set smarter revenue targets

After you learn what the break-even point is, revisit the company’s revenue targets to ensure they’re making a profit. Knowing this metric helps you create targets that will prevent a business from losing money.

Improve your pricing strategies

You can also discern whether a business’s pricing is working for them or if they should increase prices to stay profitable. Diving into a break-even analysis, you might also find that the company can lower prices, making them more competitive so they can sell more units and increase revenue.

Secure funding

Whether it is a startup creating a business plan to attract investors or trying to get funding for a new project, the break-even point is used to demonstrate how a business will be successful to potential investors or lenders.

Why the break-even point matters

A business may have a high volume of sales, but that doesn’t mean it’s profitable.

Understanding the break-even point helps companies stay on track and avoid spending decisions that could lead to losses.

For example, let’s look at the consulting business, Kramer’s Consulting. Kramer’s makes $70,000 every month. But it also spends $30,000 on salaries, rent, business insurance, and other fixed overhead costs. Variable costs range from $32,000 to $42,000 a month.

Right away, you can see that Kramer’s could have some financial viability issues. Because sales revenues total $70,000 and fixed costs are $30,000, there’s only $40,000 remaining to cover variable costs. When fixed and variable costs equal total revenues ($30,000 + $40,000 = $70,000), then the business breaks even.

But when Kramer’s Consulting spends $42,000 on variable costs, it loses $2,000 that month. But if it spends less than $40,000, there will be profit left over.

While it looks like Kramer’s Consulting is operating on a razor-thin profit margin in some months, but then slipping into the red during others, the executive team — knowing its break-even point — can implement new strategies or business model changes that will help increase profits. These changes can include:

- Pricing strategies: By raising the price of its consulting services, Kramer’s can increase total revenues without selling a different number of units or cutting costs.

- Sales targets: Kramer’s could also decide to incentivize its sales team to hit a higher target each month, potentially leading to higher revenues and greater profits.

- Cost-cutting strategies: Another option is to look at those fixed and variable costs and see if there are any expenses that could be cut in order for the business to break even.

Kramer’s Consulting does an audit of its fixed costs and realizes its executive salaries are higher than average for the industry. The CEO, Kramer, decides to reduce his own salary, at least until the company can sustainably increase its revenue.

So long as Kramer’s Consulting calculates its break-even point, the company will continue to gain financial insights that will help it work with the numbers, budget smarter, and plan ahead in a way that will keep their profits high and their business thriving.

How to calculate the break-even point

Using the break-even point formula for a business will demonstrate how much it needs to sell to meet its costs. From that point, we can determine whether to increase the sales price or the sales volume to be profitable.

Here’s the break-even point formula:

Break-Even Point = Fixed Costs ÷ Contribution Margin

Let’s break down these two other components, so you know how to calculate the break-even point.

Fixed costs

Fixed costs are the expenses that stay the same no matter how many units the business sells. They are the overhead costs a business pays to stay operational, such as rent, salaries for managers, and utilities. Contribution margin

The contribution margin is what remains after deducting variable costs from sales revenue. This number is the sales price per unit minus the variable costs per unit.

Contribution Margin = Price of Product – Variable Costs

Break-even point formula example

Let’s look at an example of the break-even point formula in action.

Toby’s Sporting Goods manufactures tennis rackets. The company’s owner wants to know how many rackets it has to sell to break even. Toby’s company sells a tennis racket for $100, and the cost of materials and labor for each racket is $60. Plugging these numbers into the contribution margin formula, we get $40 per unit as the contribution margin.

$100 (product price) - $60 (variable cost per unit) = $40

That means Toby’s Sporting Goods has $40 left per racket to pay for the fixed costs. What’s left after that is the net profit. But, before getting into profits, we want to know how many rackets Toby’s has to sell at the sales price of $100 to break even.

Let’s say Toby’s Sporting Goods’ overhead costs for one month are $20,000. Divide the fixed costs by the contribution margin to find the break-even point.

Break-Even Point = $20,000 ÷ $40 = 500

So Toby’s Sporting Goods has to sell 500 tennis rackets every month to break even. If sales are slower, the company starts losing money. Anything over 500 rackets is where the net profit starts.

Need help determining fixed and variable costs? BILL tracks all your accounts payable so you know how much you’re spending every month paying suppliers and vendors. Try BILL today!

What’s a break-even analysis?

When you want to know if a new product, project, or other initiative will be profitable, do a break-even analysis.

A break-even analysis shows how much is required to sell to cover costs. Aim for a break-even point or higher. But the bottom line is this: know the minimum number of units sold or sales revenue that is needed to break even.Then, every additional unit sold is profit for the business.

Here’s another example: let’s say a business wants to release a new product. It plans on selling each unit for $20, but needs to know how many units they have to sell to break even in one year.

To perform the break-even analysis, start by calculating variable costs.

Let’s use a hypothetical situation where a company expects to produce 1000 units for the year at a cost of $12,000. Dividing the total variable costs by the number of units, we can determine the per-unit variable cost: $12,000 / 1000 = $12.

Now you can find the contribution margin. We know that the contribution margin is the difference between the sales price of the product and variable costs. So, if the new product per unit sells for $20, and the variable cost is $12, the contribution margin is $8.

Next, you need to look at fixed costs to determine the break-even quantity. For this new product, you estimate that the fixed costs for the year will be $10,000. Using the break-even formula, we can calculate that the business must sell 1,250 units in a year to break even.

Number of Units to Break-Even = Fixed Costs / (Sales Price Per Unit – Variable Cost Per Unit)

$10,000 / ($20 - $12) = 1,250 units to break even

Now they must sell 1,250 units to break even, but the business was only planning on producing 1000 units.

There are two options. Increase the selling price by $2. At $22 per unit, this breaks even.

$10,000 / ($22 - $12) = 1000 units to break even

Alternatively, option two is producing more units without lowering production costs. Or, a potential third option, which is to examine how to reduce fixed costs. As long as total fixed and variable costs equal total revenue, the company will break even.

Doing an analysis helps determine what pricing and spending decisions make the most sense for a business so that they make sufficient profit — all by simply determining the break-even point.

Help your small business stay profitable with better financial management

There’s a lot to managing accounts and making strategic decisions for any company. But with the right tools, it’s easier to track costs, keep finances in order, and make decisions that will help the company stay profitable.

BILL can handle all your payments and keep your payables and receivables in one place. Learn more about how BILL can help your small business today!