Many small businesses use the same account for personal and business transactions. While it seems more manageable, the truth is that it makes tracking your finances and managing your end-of-year taxes much more difficult.

No matter the size of your business, you should never combine your business banks account with your personal bank account. Besides making organizing your transactions more challenging, you’ll also miss out on benefits like discounted interest rates and higher percent cashback.

What is business banking?

“Business banking” refers to the financial services banks offer business clients. These services might include:

- Business checking accounts

- Interest-bearing savings accounts

- Business savings accounts

- Access to lending services

- And more

Also called commercial banking, business banking offers exclusive benefits tailored to small-to-medium-sized businesses. For example, a bank may provide a high percentage of cashback for business credit accounts or charge a lower interest rate for loans.

So, when should you start your business banking account? As soon as you begin spending or accepting money. You can choose from business checking accounts, savings accounts, and business credit cards.

Business checking account

A business checking account comes with a business debit card, so these types of accounts are typically reserved for day-to-day transactions like deposits, bill payments, and purchases.

Business savings account

As its name suggests, a business savings account allows you to save money for future business usage. You’ll want to use your savings account to store funds and enable them to grow over time.

If you’re looking for an even greater return, you could opt for an interest-bearing savings account, so the bank deposits interest into your account.

Business credit card

Business credit cards are a great way to build credit, improve cash flow, and enjoy bank-specific rewards and benefits. But keep in mind that, like a personal credit card, you’ll want to pay off your balance every month before interest is tacked on.

Key takeaways

- Business banking is a set of financial products and services a bank provides to a company or organization.

- Business banking includes checking and savings accounts, loans, and credit which are explicitly tailored to businesses.

- This type of banking allows you to organize your finances, track your business expenses, and easily file your taxes.

Breaking down the benefits of business bank accounts

Companies, partnerships, and sole traders need a business banking account as part of their financial strategy. Here are three ways that having a business bank account can help you operate better:

Benefit #1: Have a better grasp of your expenses

Financial management is essential for business owners, and business bank accounts help you keep track of your business expenses and investments. You can organize your receipts and payments in your business bank account to ensure you are paying all the right bills on time.

A business account helps you avoid mixing personal and business fees and expenses. You can get a better picture of your company’s financial situation, thus allowing you to plan and take better advantage of opportunities in the marketplace.

Benefit #2: Appear more credible and professional

Your business banking account reinforces your company’s image, which can help attract new customers or finance sources. When people see you using a commercial bank account, they automatically assume that the company is a legitimate enterprise.

Benefit #3: Easier tax filing

Mixing personal and business funds makes it harder to file your tax returns. If you have to sort through all these transactions, it becomes more difficult to file because you need to find out which are business or personal expenses.

Banking separately for your business makes filing your taxes easier at the end of the year. Additionally, you’ll be able to find deductions for your business and reduce your tax liability.

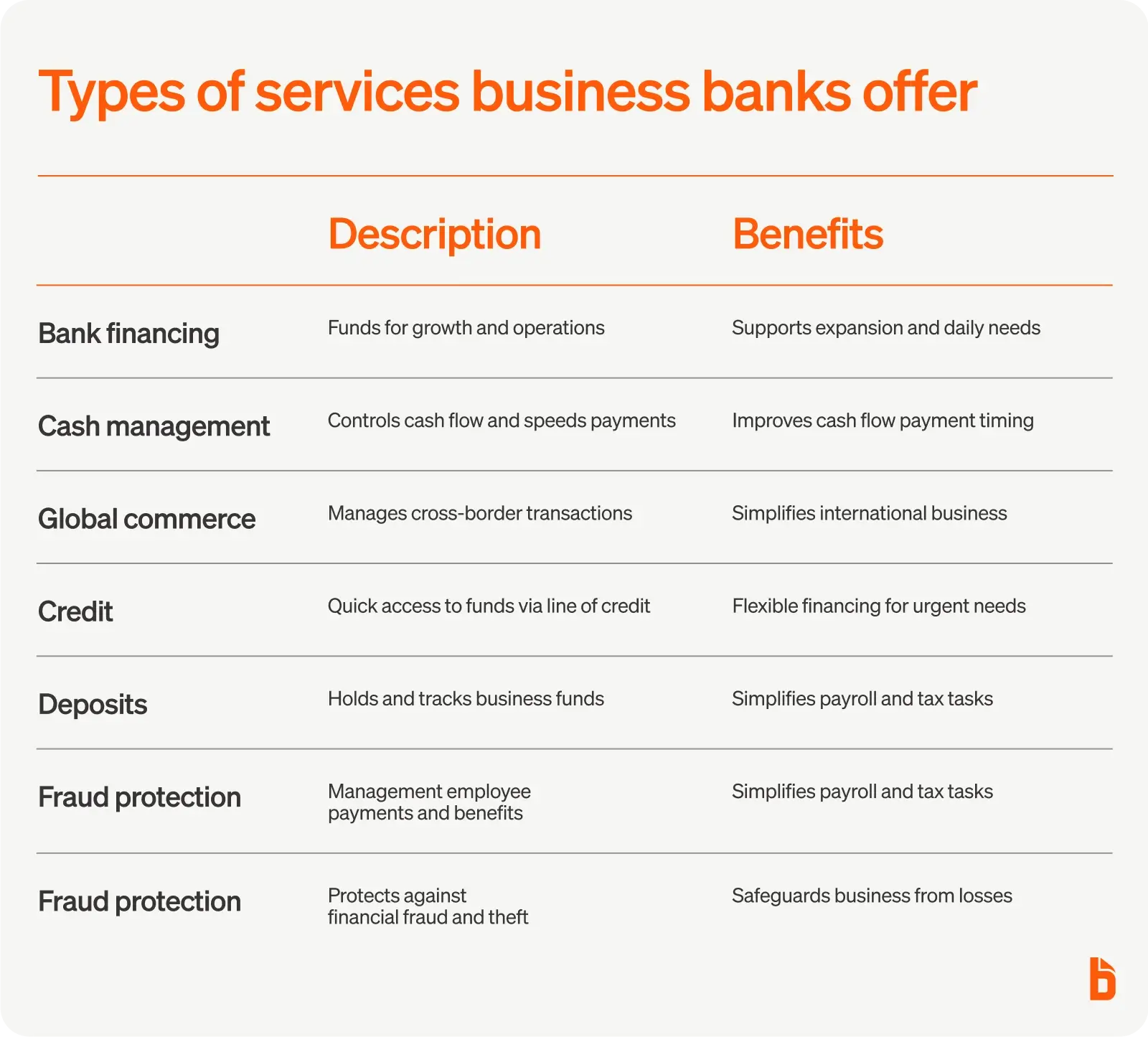

Types of services business banks offer

Business banking is essential in setting up a new business, but navigating the different financial products can be challenging because you need to understand what each service offers and how—or if—it can help you.

Bank financing

Financing is one of the most popular banking services among business owners. Financing assists your company’s growth and development by providing the needed resources to expand.

You can use the funding to expand your business by purchasing products such as inventory, machinery, or other equipment. Bank finance can also help you pay employees on time, repair or improve your building, and attend to your customers’ needs.

Cash management

A cash management account is a business bank product that assists you in controlling your cash flow. Cash management accounts help you reduce the time it takes to send and receive payments, track your accounts payable, and monitor the minimum balance in your business checking account.

Cash management services include access to Automated Clearing House (ACH) and electronic funds transfer services that help speed up the processing of payments. These services are essential because they allow you to predict when incoming cash will arrive.

Global commerce

A global commerce business bank account helps you manage invoicing, payments, and financial transactions across different countries. This service also covers businesses from fluctuating exchange rates and trade barriers.

Credit

When your business needs additional financing, apply for a business line of credit. Lines of credit usually have a higher interest rate than a business loan, but the pro is that you can access it quickly if you’re in a pinch.

Deposits

A business bank account can hold funds that customers, employees, and investors deposit. You’ll receive a statement of your deposits regularly and electronic statements that include transactions, balances, and transactions on websites.

A dedicated business checking account can help you pay bills, transfer funds, or settle cash balances. Businesses may also use a non-current account to earn interest on their account balance.

Payroll

Most banks offer payroll management services to help you simplify your payroll tasks. Payroll services include:

- The deposit of employee pay cheques

- Sending AHC payments to employees’ bank accounts

- Reconciling payroll information

- Managing benefit plans

Paying employees can be tricky for small business owners when calculating taxes and delivering the right amount on time, so payroll services can help simplify any confusion.

Fraud protection

Fraud has become a massive issue in the business world. In fact, credit card fraud is the leading cause of identity theft in the United States, and businesses are only as protected as their banks.

Bank and employment or tax-related fraud are not too far below. So, even if you do your best to cross your Ts and dot your Is, fraud and identity theft can happen to anyone.

Fortunately, nearly all U.S. banks offer fraud protection services that help protect your business from financial losses due to fraud and identity theft.

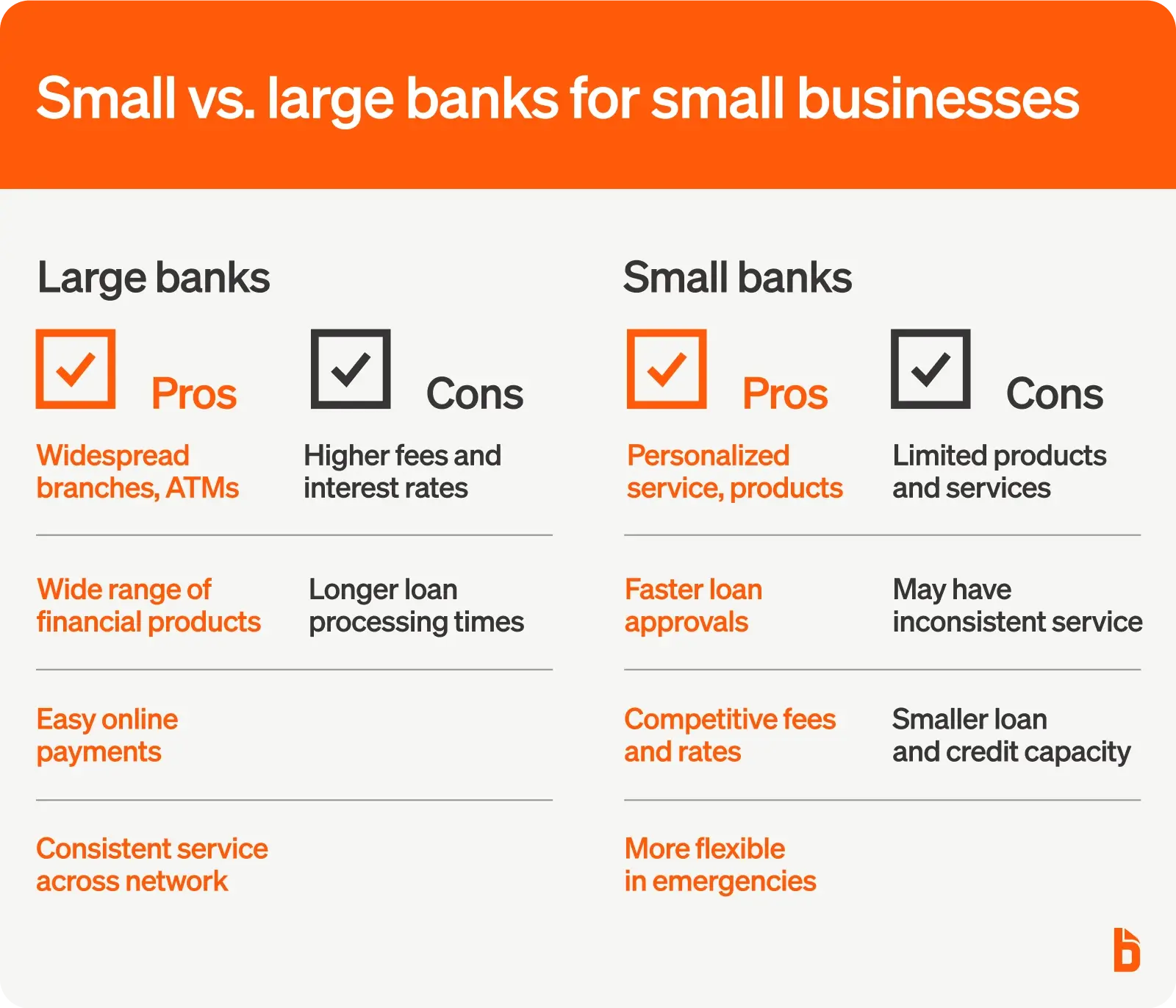

Small banks vs. large banks for small businesses

While some big banks provide financial services with great benefits, it ultimately comes down to what you’re willing to compromise on. Less competitive rates and higher fees are often tradeoffs for comprehensive products and services.

Smaller banks have a more personal relationship with their customers and are more likely to make accommodations in an emergency. Plus, local small banks and credit unions often invest in their own communities, so it can feel like you’re working together to improve your area’s economy.

However, you might save money in the long run and get better benefits from large-scale banks. Let’s break down the pros and cons of both.

Large banks pros

- Widespread branch and ATM access

- A broad selection of financial products

- Easy to set up automatic payment methods thanks to an online business bank account

- A uniform service standard across the network

Large banks cons

- Higher fees and interest rates

- Longer processing times for loans

Small banks pros

- Personalized service and products

- A faster loan approval process

- Competitive fees and interest rates

- May be willing to negotiate on loan principal and interest during a cash flow crunch

Small banks cons

- Limited products and services

- They may not offer the same standard of customer service as big banks

- They may not be able to provide very substantial loans or credit lines

Choosing a bank for small business management

Unfortunately, some banks don’t make their fine print easy to read. With these account features, you can choose a reliable bank that provides all the services you need to run your successful business.

Consideration #1: Bank size

A large bank like Bank of America will likely have more employees, which means it has a more comprehensive selection of products and services. The downside is that its customer service may be less personal.

On the other hand, smaller banks are less likely to offer the same products and services. However, the staff is more likely to be able to provide personalized service.

Consideration #2: Business loans and credit

Credit is an integral part of banking for most businesses. It’s not uncommon for small businesses to get a loan from their business bank to fund the purchase of their company’s first office or a new piece of equipment.

Larger banks usually have many businesses applying for loans, so they’re less willing to go the extra mile to help you. Smaller banks are more flexible and accommodating to new and smaller companies.

Consideration #3: Interest rates

Banks have different interest rates on their business checking and savings accounts. You’ll have to do additional research to determine which bank offers the best interest rate according to your situation.

For example, you'll be quoted a high interest rate if you have low savings. But if this is your first time borrowing and you have a healthy cash flow, you might get a lower and better rate.

Higher interest rates on your interest-bearing checking and savings accounts mean your money can grow and compound significantly over time. Balance these rates with the potential fees you would pay to maintain your funds to get a better picture of your returns.

Consideration #4: Service fees

One of the biggest complaints businesses have about banks is their excessive fees. These fees may include the following:

- Monthly maintenance fees

- ATM fees

- Overdraft fees

- Excessive cash transactions fees

- Wire transfer fees

If you want to pay less for your bank services, you should look for a bank that does not charge high fees. Avoiding overdrafts and out-of-network ATM fees can also be a huge money saver for your business.

Consideration #5: Physical location

Banks are more than just financial institutions. They’re social organizations that serve the needs of their local communities with products that provide security and convenience.

The nature of your business will determine how important the location of your brick-and-mortar bank is. For example, it may be best to bank at a branch nearby if you need to make frequent deposits or withdrawals. Traveling business owners may require a bank with units in several states.

Consideration #6: Business banking services and features

Once you’ve narrowed down the list of banks to those most relevant to your business, you’ll need to pick one that offers the best services for your company. Think about what products and services you need most.

For example, consider how convenient it will be to access your account information online or through a mobile banking app. Can you set up automatic bill payments? You need a reliable way to access your account and keep track of your transactions at all times.

Consideration #7: Perks and benefits

Many banks offer special perks and benefits to entice new business owners into opening accounts with them. These benefits may include the following:

- Free training and courses to help your business succeed

- Bill payment services for your business’ utility and credit card expenses

- Online banks allow 24/7 access to your company accounts

What do I need to open a business bank account?

Once you’ve picked your bank, opening a business bank account is easy — in most cases, all you need is a few pieces of information:

- Your Employer Identification Number (EIN) or Social Security Number (SSN) if you’re a sole proprietorship

- Your business formation documents, which you must file with your state to legally register your business

- Your ownership agreements to confirm your ownership

- Your business license, which is a legal requirement and can be applied for through your Secretary of State

Keep in mind that some banks may also require extra steps: Some may request that you supply the articles of incorporation or certain IRS forms. Most banks will require a minimum deposit as well. Always check the bank’s register requirements before opening a business account.

How to use business banking to your advantage

Setting up the right business bank account is an excellent start to mapping out your company’s financial strategy, but how you use it can make a big difference in the long run.

Here are three ways that operating a business bank account can help your company:

1. Never worry about tax season again

One of the last things any business owner wants to think about is filing taxes. Unfortunately, taxes are here to stay, meaning you need to know how to read and utilize your business bank account to file properly.

A handful of new changes come with filing taxes as a business, from self-employment tax rate and making estimated quarterly payments to new tax standards you’ll be required to meet.

Using a business bank account will make it easier to file your taxes as you’ll have all your business and personal expenses separated. This account can help you budget better, keep track of cash flow, and plan.

2. Use your perks towards expanding your business

As a business owner, you’re starting from the bottom and making your way up, meaning that upgrades and increased cash flow will come with time.

But a business checking account can provide rewards—like lower interest rates and cash back—that can help better your cash flow and position your business on the road to success, especially since 82% of businesses fail due to cash flow issues.

Take advantage of your bank’s perks to earn extra cash for your business, whether it goes directly into savings, new hires, or upgrading your office space.

3. Build better credit

If you open a business checking account, you’ll also have the option to open a credit card. Credit cards in business can be great when used properly and paid off on time. When you do that, your business credit score will increase, and you can grow in many ways.

For example, banks determine your interest rates depending on your score. Money saved on interest can help grow your business and improve your line of credit when you’re ready to expand. You’ll also have better chances of getting approved for larger business loans and better terms from suppliers.

Track all of your transactions with ease

Business banking is specifically tailored to business owners—so whether you’re just starting or relying on your personal account, now is the time to make the change.

In doing so, you’ll be able to manage your financial needs more effectively and better organize your business finances and cash flow while reaping the rewards that come with these types of accounts.

But “managing” is an umbrella term that could mean a thousand different things, which is why any business needs to be able to rely on an accounts receivable and payable management system like BILL. We’ll help you keep track of all your business banking accounts—from AR to AP and everything in between.

Learn more about what BILL can do for you today.