Businesses incur two types of costs when creating their income statements: Overhead costs and operating expenses. In a two-step income statement the operating expenses are aligned at the top underneath revenue to calculate gross profits and then followed by overhead expenses to calculate the net operating income.

The key points: Overhead costs vs. operating expenses

Overhead costs and operating expenses are categorized differently because it’s easier to gain clarity on where you’re spending your money. Familiarize yourself with these expenses to see where your money is going and determine how you can cut down on unnecessary costs without sacrificing the quality of your products and services.

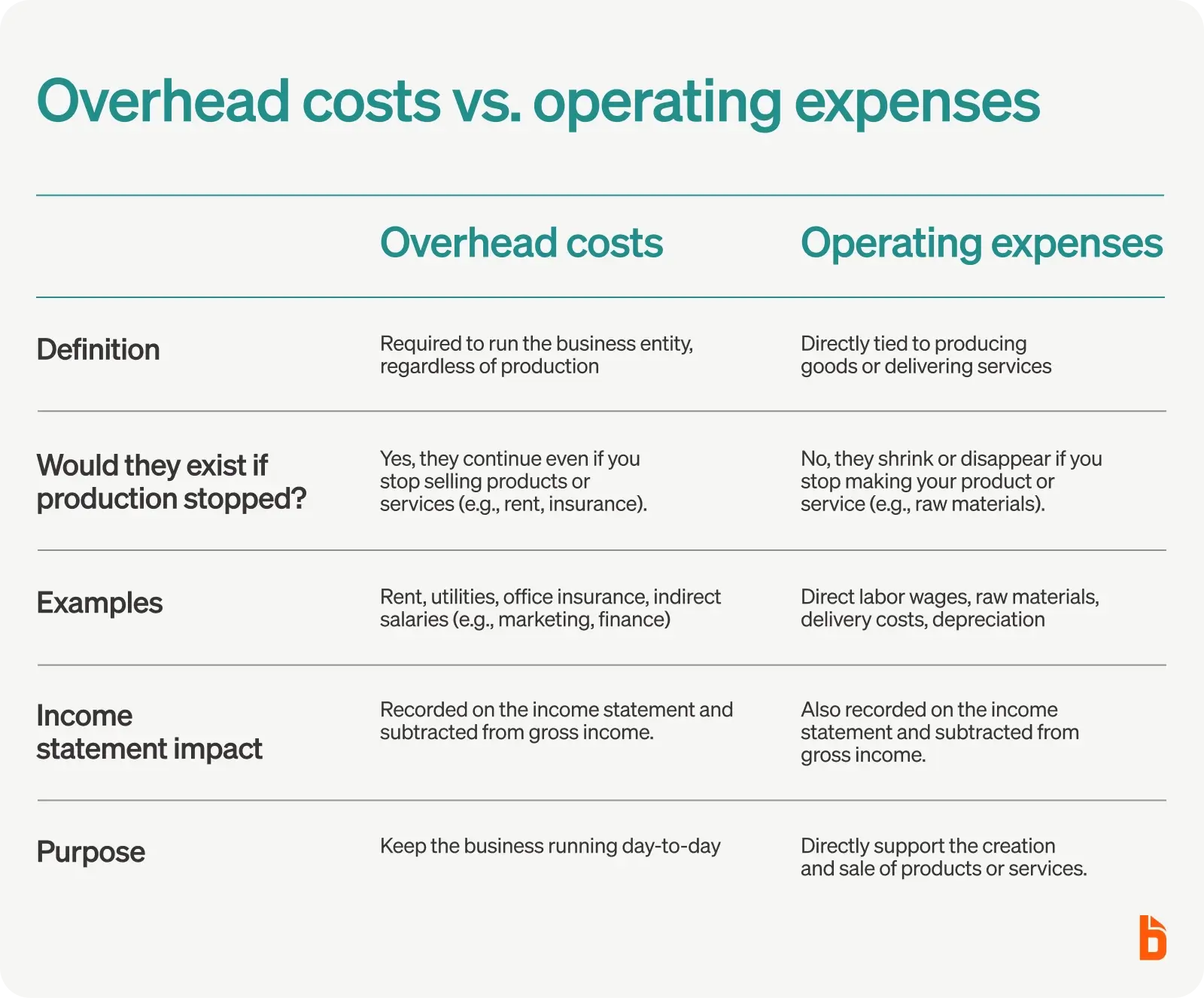

The easiest way to tell the difference between overhead costs and operating expenses is whether one of these costs would disappear, or be greatly reduced, if a business stopped making its product or service.

For example, if a clothing store stopped selling clothes, its operating expenses would shrink because no material is needed. But just because the business owners stopped selling their products doesn’t mean they don’t have overhead costs, like rent, to pay out.

So, what does this mean? Operating expenses don’t exist without daily operations related to what you offer. But overhead costs will exist as long as your business entity exists. That’s not all, though: Let’s break down the three main differences between overhead costs and operating expenses.

- Overhead costs are required to run the business and cannot be avoided, while operating expenses are needed to perform services and create products.

- Standard overhead costs include rent, utilities, and insurance payments, while operating expenses may include salaries, depreciation, and delivery charges. Note that some operating expenses could also be considered overhead costs—and the categorization depends on the situation. Salaries for direct labor, like a cashier, would be an operating expense. On the other hand, salaries for someone in marketing or finance would be indirect and considered overhead.

- Operating expenses and overhead costs are both recorded on an income statement—or a profit and loss statement—and subtracted from the gross income to find the bottom line. This number tells owners what profits they’ve seen that month, quarter, or year.

What are overhead costs?

Overhead costs—also called non-operating or indirect costs—refer to the ongoing expenses that support a company’s operations like rent and utilities.

In other words, a business must pay overhead costs to stay open and operational.

Think of it this way: While overhead costs are expenses that occur “behind the scenes,” no business can operate without them. That means any sized company can have overhead costs—in fact, they’re standard costs that every type of business will encounter as a first step to becoming operational and profitable.

Understanding your overhead costs as a business owner is essential. It helps you do two critical things:

- Maintain a healthy and accurate budget

- Assist in determining how much you should charge for your products/services

After all, your income needs to be greater than your expenses to generate a profit. And overhead costs help determine how much you’re spending, which shows you how much you need to sell (volume), and at what price point to be profitable.

But what exactly are overhead costs, and how do they differ from everyday operating expenses?

Types of overhead costs

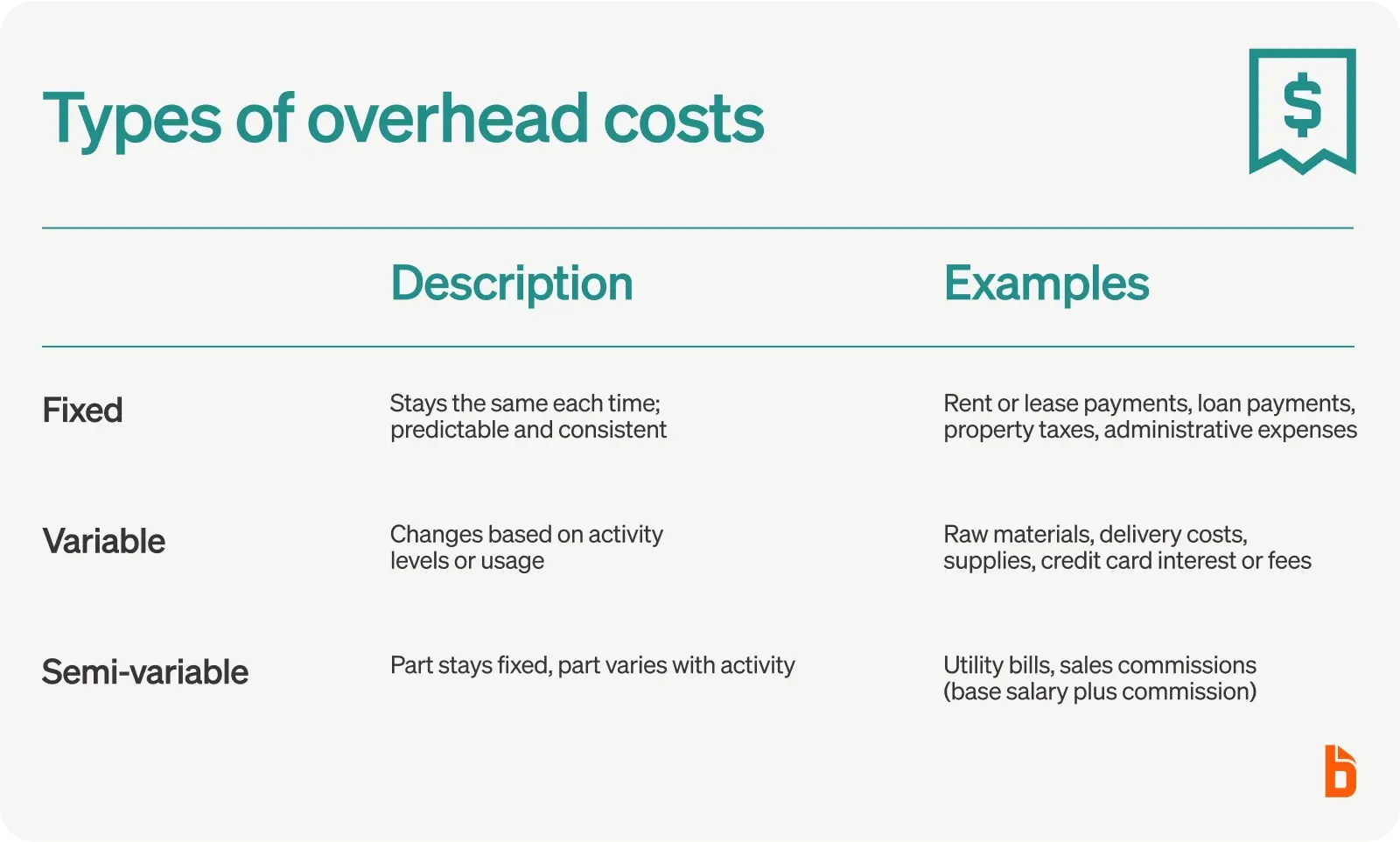

Generally, these overhead costs are divided into three main categories: fixed, variable, and semi-variable. Let’s break down the differences between these three.

Fixed

Fixed costs are the same dollar amount every time they occur. They are consistent expenses you can expect to pay monthly, quarterly, or annually.

Some of the most common fixed costs in a business include:

- Rent, mortgage, or lease payments: These payments don’t change because the amount you agree to pay is contractually-binding. Only at the end of your rental period or mortgage agreement can adjustments be made.

- Loan payments: Your loans include interest, which might be variable, but the repayment amount will remain fixed if you’re paying off a traditional term loan.

- Property taxes: Property taxes depend on your property’s worth, updated yearly.

- Administrative expenses: Administrative expenses, like phone lines or supplies, are considered overhead costs.

Variable

Variable costs don’t always stay the same but change based on activity levels. For example, your credit card interest may increase for one statement if you spent a lot on it last month and didn’t repay the balance in full.

Typical variable costs include:

- Raw materials: Your expenses may fluctuate depending on seasonal trends and popularity.

- Delivery costs: These costs depend on weight, size, and requested shipping speed.

- Supplies: Prices are determined by general supply and demand rates.

- Credit card fees: Interest fees depend on how much you spend.

Semi-variable

Semi-variable costs are unique because they are part-fixed and part-variable. A portion of this expense remains the same, while the other part might change depending on activity levels.

Here are some of the most common semi-variable costs a business incurs:

- Utility costs: Utilities, like electricity, will vary because part of the cost remains the same—the delivery and production cost—while the other part of your bill hinges on your monthly usage.

- Sales commission: A salesperson getting a commission will have a base salary plus an additional amount depending on how much money they’ve brought in that week, month, quarter, or year. Commission may be considered part of a sales and marketing overhead cost on the income statement.

Where are overhead costs are recorded?

Overhead costs go on the income statement. Along with operating expenses, overhead costs are subtracted from the gross income to arrive at the net income figure, which shows business owners the company’s profitability.

Calculating overhead cost ratio

Overhead costs go hand-in-hand with operating expenses and interest income. Alongside operating and overhead, interest is one of the most significant expenses on an income statement, which is why both are included in the overhead cost ratio formula.

The first step to calculating your overhead cost ratio is to add all of your operating expenses together and then divide that number by the combined figure of the operating income and net interest income:

Overhead ratio = operating expenses / operating income + net interest income

Let’s break down each part of this formula:

- Your operating expenses—which we’ll cover in the next section—include costs that are integral to the daily operations of a business, like salaries.

- Taxable net interest income is the difference between what you owe and what you’ve paid in interest. To get this number, you need to consider how much a business receives interest and how much it pays off through the net interest margin formula.

- Operating income is the company’s earning capacity from manufacturing goods and services. This is determined by deducting the operating expenses from the gross profit.

So, if a small business called K & S Liquors has $20,000 in monthly sales, $6,000 in operating expenses, and a taxable NII of $3,000, then the overhead cost ratio is 15.4%.

Generally speaking, the lower the percentage, the more effective your business utilizes its resources. A good rule of thumb is not to exceed 35% of total revenue.

We can see here that K & S Liquors is well under 35%, which means they’re on the right track. But they live in a tourist town—so when it’s wintertime and fewer customers visit, they may need to make some adjustments to cut overhead costs.

Cutting overhead costs

One of the most common things business owners ask is, “How can I cut my overhead costs?” because these costs can add up quickly. Luckily, there are a few things you, as a business owner, can do to cut your costs.

Start by asking yourself:

- What’s costing you money—and where can you compromise? For example, you may be able to compromise on your office space if you downsize or switch to remote work.

- Could you outsource non-core work? For ongoing assignments that don’t require full-time work, like web maintenance or bookkeeping, you could consider hiring a freelancer or ad-hoc contractor.

(When making major financial decisions like these, don’t forget to conduct a cost-benefit analysis. Performing a CBA will help you determine whether a potential project or idea will benefit your business in the long run.)

What are operating expenses?

Operating expenses—sometimes abbreviated as OPEX—are the costs that affect a business’s daily operations and directly go towards producing products or services.

Think of what affects a business’s ability to create products. If a pizzeria needs to make pizza, then they need workers (wages), ovens (equipment), and plenty of dough, sauce, and toppings (materials). The cost of these things is the operating expenses that help continue the pizzeria’s production.

Understanding your operating expenses is crucial when it comes to evaluating the financial health of your company because it can:

- Help assess your cost and inventory management efficiency.

- Highlight the level of costs that you need to make to generate a profit.

- Tell you what you need to put money toward to keep running—and, in the same vein, what you can spend less on.

Where are operating expenses are recorded?

Operating expenses appear on a company’s income statement and are recorded as part of the cost of goods sold (COGS). Knowing the COGS helps managers and accountants estimate the company’s bottom line—if the COGS increases, they know the net income will decrease.

Types of operating expenses

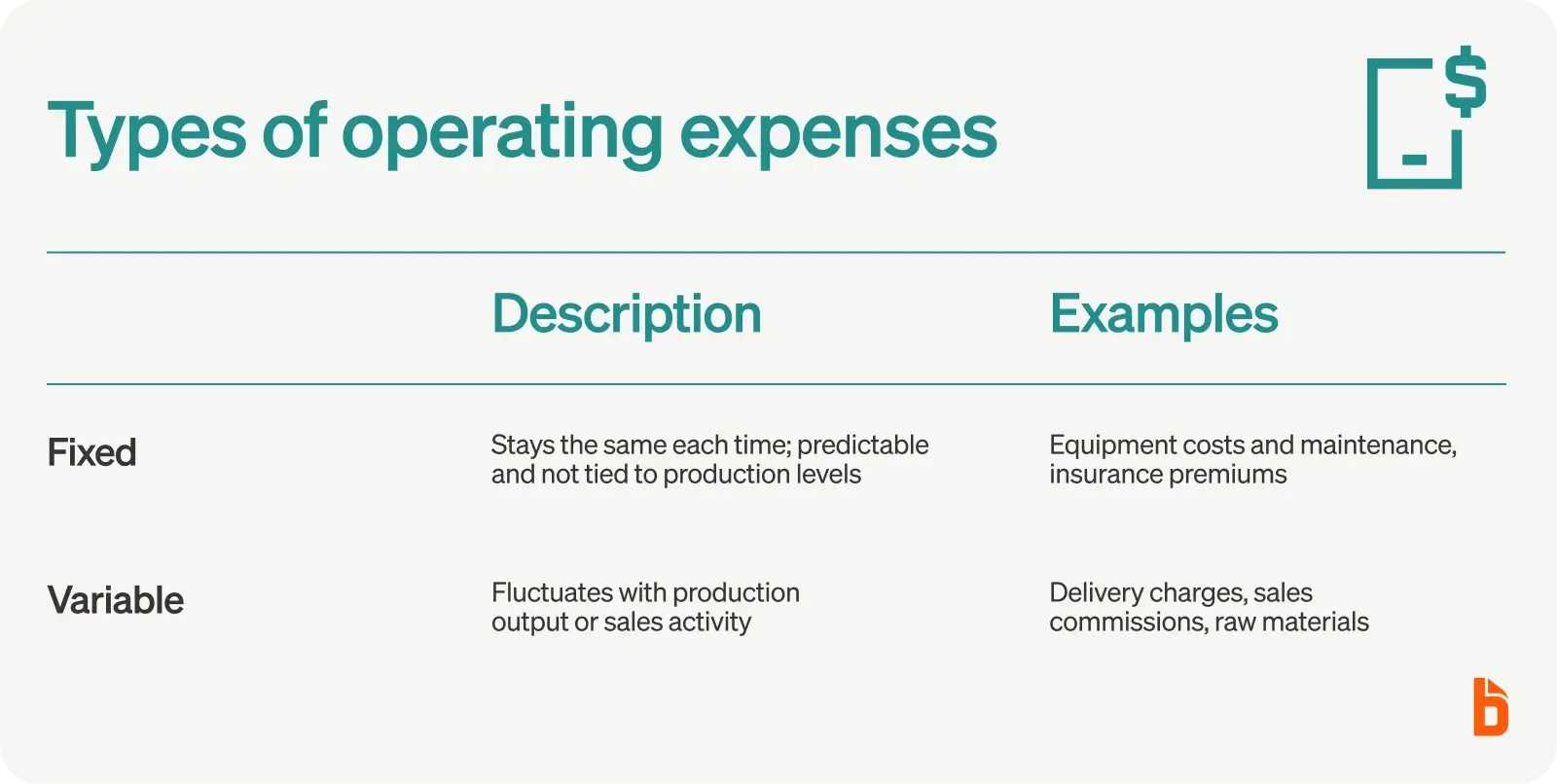

Unlike overhead costs, operating expenses only focus on two types of expenses: Fixed and variable.

Fixed expenses

As you know, fixed expenses are the same every time they’re billed to you. Regardless of your usage activity, these expenses stay the same and hardly affect production cost estimates since they are so predictable.

Since you have to pay fixed costs no matter how much you sell, you should be careful about what you add to the list of your fixed expenses.

Here are some of the most common fixed operating expenses:

- Equipment: Equipment is the heart and soul of producing products, whether a pizzeria or a manufacturing plant. With this cost, you also have to keep equipment operational, safe to use, and up-to-date on maintenance.

- Insurance payments: Insurance premiums are fixed packages that last from six to twelve months (you’ll have the option to renew, which means the value may change).

Variable expenses

Variable expenses depend on output and production changes, meaning they fluctuate depending on how much you’re using.

This is similar to the variable costs you might find in your overhead budget.

However, variable expenses affect the business more daily if they’re directly related to your sales volume.

Here are some common variable expenses you may incur:

- Delivery charges: Delivery charges and shipping costs vary depending on how much you order per shipment.

- Sales commission: Sales commission was previously mentioned as a semi-variable overhead cost, but it could also be a variable operating expense. Since commission is compensation paid by the employer to the worker for obtaining sales, it may be listed as an SG&A expense (selling, general, and administrative) on the income statement.

- Materials: In business, “materials” refer to whatever you need to create and sell. Materials could be the ingredients of a pizza or tools for an auto body shop—whatever they are, materials are a necessary operating expense that allows you to perform a service.

Calculating the operating expense ratio

Knowing that operating expenses are determined by costs that come from everyday operations, we can move forward and understand that these include costs like COGS, raw materials, and maintenance—all of which focus on total revenue.

Operating expenses and the cost of goods sold are two different items businesses incur while running their daily operations. These costs can be recorded on a company’s income statement as separate line items, but they will eventually be subtracted from total revenue or sales for the period in question.

That’s why, to find your operating expense ratio, you need to divide your total operating expenses by your total revenue.

Let’s say that K & S Liquors has $6,000 in operating expenses during June and $10,000 in total revenue. Using this formula, K & S Liquors has an operating expense ratio of 60%.

The good news? 60% to 80% is a normal range; the lower the ratio, the better your business utilizes its resources.

That means that K & S Liquors is doing great this month—but if prices fluctuate during the non-busy months, they may want to consider cutting operating expenses.

Cutting operating expenses

If you’ve calculated your operating expenses and the number made you take a step back, don’t worry—there are things you can do to cut your operating costs. Most small businesses take a look at their profit and loss statements, consider negotiation, and even downsize where necessary:

- Are you spending money on non-essentials? You might be surprised to see non-core or recurring expenses that you didn’t realize were there—then, you can determine what’s essential and what’s not.

- Can you negotiate your expenses? Creditors, for example, will often supply payment plans with low to no interest rates if you’ve fallen behind on payments.

- Is there anywhere you can downsize? One of the most prominent mistakes startups make is opting for a fantastically large office when many startups are better off beginning at home or conducting their work virtually with remote work.

Stay on top of all your costs with BILL

Knowing how overhead costs and operating expenses work together—and independently—is essential. Familiarity with these costs allows you to evaluate whether you’re overpaying in expenses or drowning in expenses versus income.

You might notice a theme here: Recognizing whether you’re paying too much against your income is critical to good accounting. Luckily, there’s an easy way to keep track of your operating and overhead expenses.

BILL Spend and Expense is expense-tracking software that helps you manage all your expenses, no matter how infrequent or semi-variable they may be. Stay on top of what you have to pay every month, quarter, and year so you can focus on what’s most important: Doing business.