There's a good chance you've either sent or received an ACH credit without knowing it. Often used for utility bills, payroll, and even the direct deposit of tax refunds, ACH credits are favored for being a secure and reliable way to send money directly to someone's bank account.

If you want a dependable payment method that takes out the intermediary, the answer could be ACH credits. Here's what you need to know before you get started.

What is an ACH credit?

An ACH credit, often called an ACH deposit or direct deposit, is a payment "pushed" from one bank account to another using a US banking network known as the Automated Clearing House Network (ACH network).

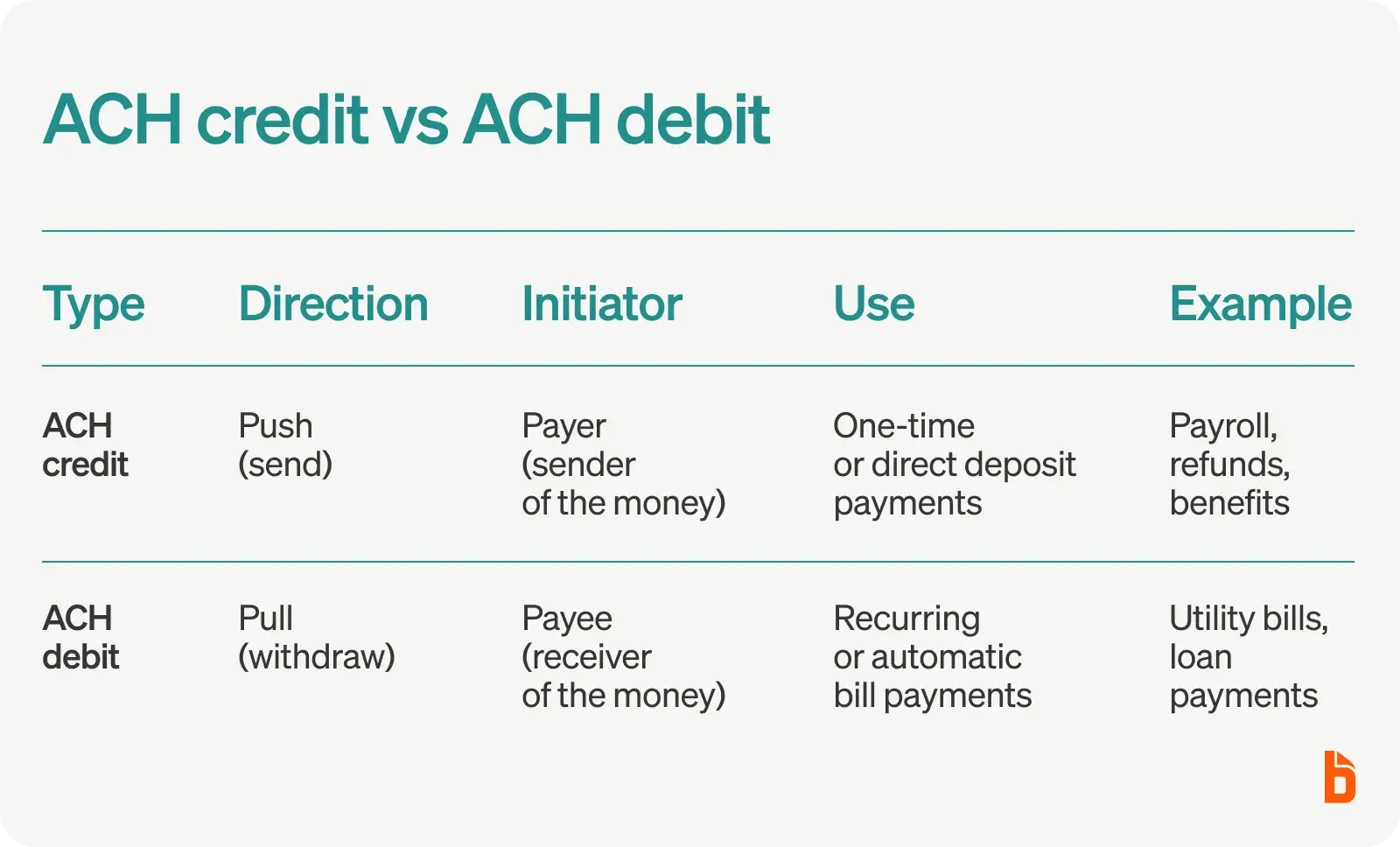

ACH credits are push transactions. This means the person making the payment pushes the money from their bank account to someone else's.

A typical example is using ACH credits for payroll: the employer pays employees by "pushing" electronic payments into their checking accounts.

In addition to paychecks, ACH credits can also include government benefits, refunds, or withdrawals from payment services like Venmo.

ACH credit vs ACH debit: What is the difference?

ACH credits are one of two types of ACH transfers, the other being an ACH debit (or ACH withdrawal).

While ACH credits are "push" transactions, ACH debits pull funds in. In other words, the person making a payment allows the person they're paying to withdraw money from their account.

ACH debits are commonly used for recurring payments like electric bills and mortgages. The payer gets the convenience of automatic payments from their checking account every month, and the receiver doesn't need to process manual payments.

If you're sending money, you'll likely use an ACH credit. But if you have a supplier or vendor you make regular payments to, they might ask you to set up ACH debits to make processing the payment smoother with no lift on your end.

How do ACH credits work?

Every Automated Clearing House payment (ACH payment) runs through the US clearing house system, a network of United States financial institutions. The network includes the Federal Reserve and is overseen by the National Automated Clearing House Association (NACHA). The ACH network is primarily used to make domestic electronic payments between US banks and credit unions.

Each person or business has to authorize the funds transfer. This includes the party making the ACH payment and the party receiving the money. You can only move money to or from someone else's bank account with their permission. In addition, many authorization forms allow the payer to take money back if they send too much in error.

Once the authorization is complete, whoever is initiating the ACH payment instructs their financial institution to either push the funds out (an ACH credit) or pull them in (an ACH debit). This can be done manually or set up as a recurring transfer.

Behind the scenes, the originating depository financial institution batches all of its ACH transfer requests together and sends them to a clearinghouse that verifies the transfers. The clearinghouse then sends each transfer to the receiving depository financial institution.

How long does ACH credit take?

ACH credit transfers can be processed in one to three business days (the ACH network isn't active on weekends or holidays). Some financial institutions will offer same-day ACH transfers if the receiving account is at the same bank, although this can come with an additional fee.

For example, Bank of America posts ACH transactions the next business day unless you opt for a same-day ACH transfer, which has a maximum transfer amount of $100,000.

Remember that an ACH transaction being posted and processed are two different things. Banks will only deposit the ACH credit once the funds are successfully pulled from the payer's account to avoid ACH returns.

ACH credits with higher dollar amounts are often subject to longer processing times. Banks want to avoid being left in the lurch if they deposit the funds and the transaction gets reversed due to an error.

Who uses ACH credits?

Businesses use ACH credits to deposit paychecks and benefits for workers. They also pay recurring bills and send one-time payments with B2B ACH transfers. Using ACH saves time and is more secure than sending paper checks.

Typically, consumers can only initiate ACH credits online transfers to their bank accounts. For example, someone might use ACH credit transfers when sending money from a checking account to a savings account at another bank.

Fees for ACH credit transactions

ACH credit fees are typically low, with the cost to the sender usually being less than the cost of printing and mailing a check.

There's usually no cost to the receiver, but you should know that some business checking accounts charge fees based on the total number of transactions or transaction volume.Vendors usually love companies that pay by ACH credit. They don't lose 3% of their invoice in credit card fees and don't have to deposit a check manually.

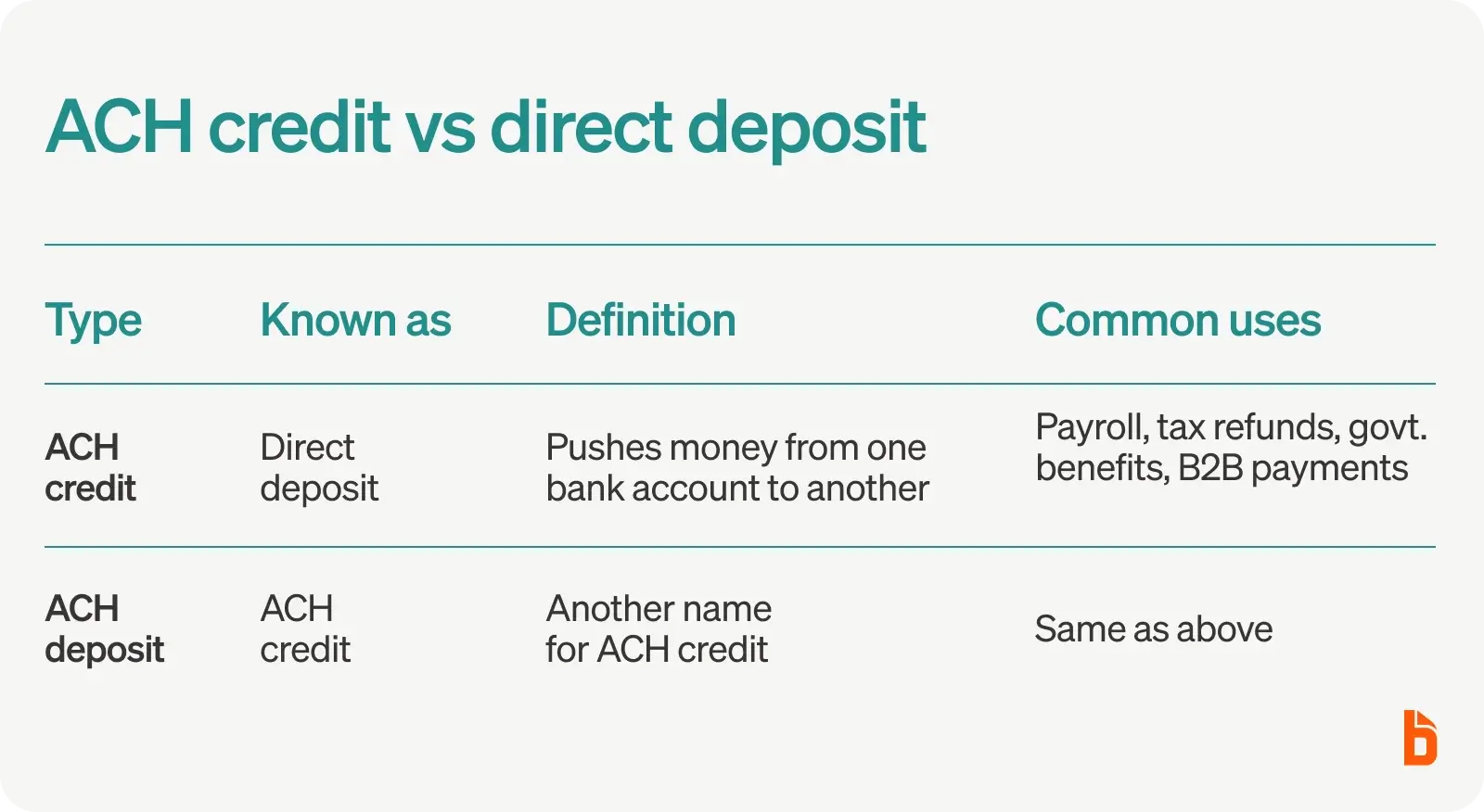

ACH credit vs direct deposit

ACH credit is the same as direct deposit. Direct deposit, or direct payment, is just another term for an ACH credit. Again, that's when your ACH transaction pushes funds out of your account.

Some of the most common types of direct deposits include electronic tax refund payments from the IRS, government benefits, and Social Security payments for retirees. ACH direct deposit is also used in business-to-business money transfers, like paying consultants or suppliers.

Make ACH credit payments with BILL

Streamline ACH credit payments with BILL, an intelligent business payments platform.BILL keeps both the supplier's and your banking information secure in the app. This means securely sending money without worrying about who can access the bank details.

Invoices can be sent directly to the system. The details get automatically entered into the platform for review, and customized workflows notify stakeholders for approval.Then, paying with an ACH credit is as easy as clicking a button.

See how BILL saves AP teams an average of 50% of their time spent on the accounts payable process.* Try BILL today.

*Based on a 2021 survey of over 2000 BILL customers.

ACH credit FAQ

What is an ACH credit transaction?

An ACH credit transaction occurs when someone initiates a bank-to-bank transfer that "pulls" money from their account to be deposited elsewhere. A common example is payroll direct deposits, where money is "pulled" from the employer's bank account and deposited into the employee's.

What is an ACH credit authorization form?

The sender and receiver must authorize the transaction by completing an ACH credit authorization form. The form covers the banking information for both parties, how much money can be withdrawn, and when the money can be withdrawn.

ACH credit authorization forms are usually created by the receiver and then passed onto the payer to fill in their information.

What does ACH credit pending mean?

An ACH credit pending means the transaction has been posted but has yet to be processed. While some ACH credits can be processed same-day, the funds can take up to 3 days to hit the receiver's bank account.

While an ACH credit is pending, the funds have likely been taken from the sender's account and are being held by either the sending or receiving bank while the transaction is confirmed and cleared.

What is ACH credit refund?

An ACH credit refund (or ACH credit return) is when the funds are returned to the sender because the transaction can't be processed. The most likely cause of an ACH credit refund is an error with the receiver's banking information, preventing the bank from completing the deposit.

Is ACH credit safe?

While not risk-free, ACH credit transactions are bank-to-bank transfers that the federal government regulates. As a result, ACH credits showed the lowest rate of fraud in a study completed by the Federal Reserve.

The risks you should be mindful of are who you're giving your bank account information to and how it's being held. Only provide your banking information to known sources and on secure channels.