All companies need to track their spending habits, cash flows, and sales performance—and automating these processes is key to reducing costs and building better financial frameworks.

With the right budgeting software solution, you can understand your business expenses, financial performance metrics, profits, and so much more. In turn, this can help to diminish costs, mitigate budget overspending, and confidently seize opportunities for growth.

What is a master budget?

No matter the types of budgets you choose to work with, the easiest way to manage them is by compiling them into a master budget sheet. A master budget is an extensive and comprehensive overview of your business’s budgets. It allows you to quickly see every aspect of your company’s financial status.

A master budget has two main components:

- Operating budgets

- Financial budgets

While master budgets are standard in larger businesses, small and medium-sized businesses can use them too. They’re especially useful if you use sub-budgets, like:

- Cash budgets

- Labor budgets

- Static budgets

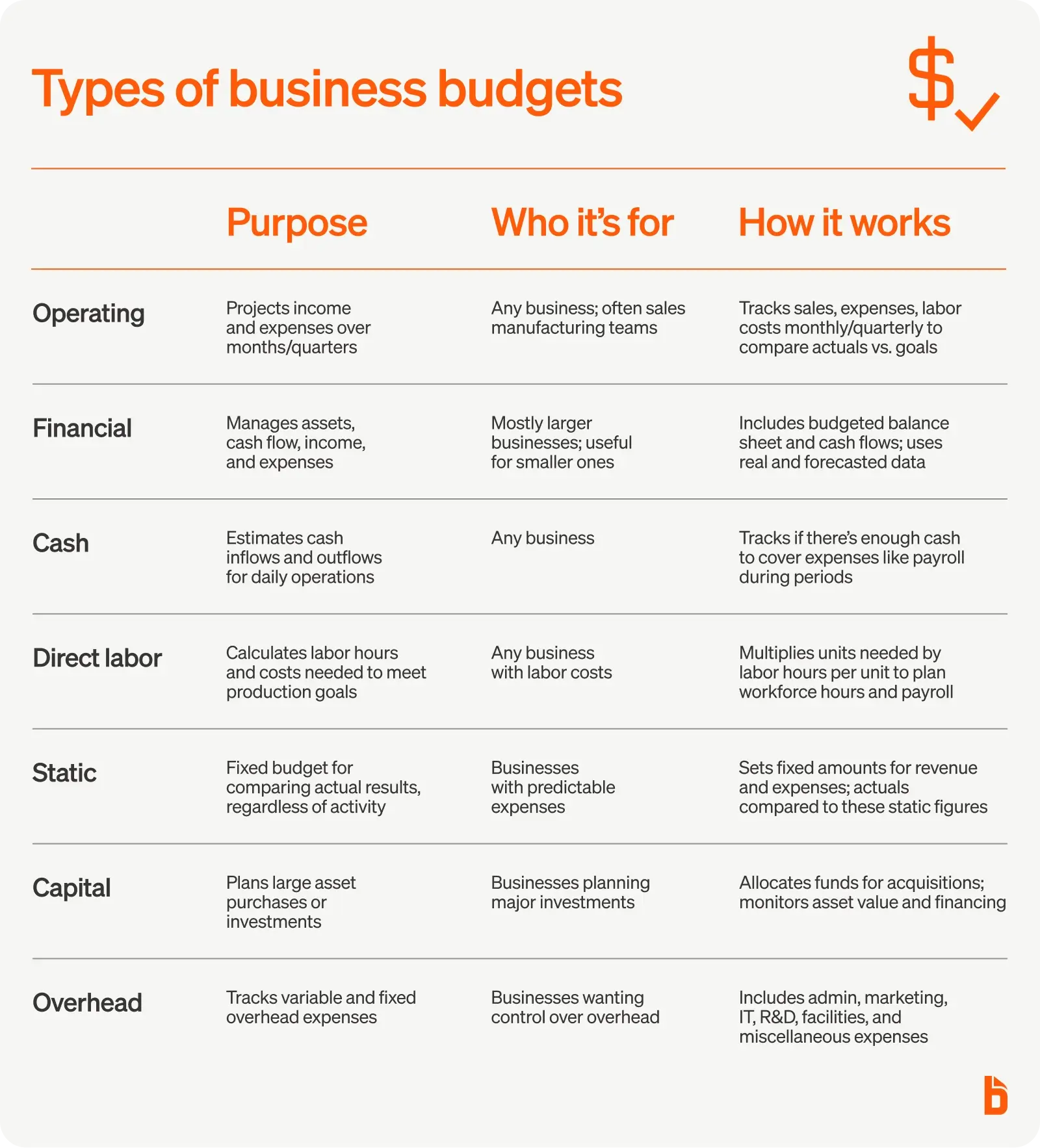

But before you get started with your master budget, you first need to work backward and create the individual budgets that apply to your company. Most businesses will need to become familiar with operating, financial, cash, labor, and static budgets.

Type #1: Operating budget

An operating budget is an essential aspect of any master budgeting plan since it provides a detailed view of a business’s expected income over the next few months to a year.

Business leaders and financial professionals will look at the results and compare them to previously-set goals for each month or quarter.

With your operating budget, you can answer questions like:

- Are sales more or less than what was projected?

- Were there any unexpected expenses?

- Does anything else need to be adjusted based on these results?

Operating budgets focus on the expenses, cost of goods sold (COGS), revenue, overhead, and administrative costs within a business.

Who it’s for…

Any-sized business can use an operating budget, but it’s typically reserved for sales and manufacturing departments. This is because the focus is on setting financial goals and then analyzing results to see if those goals were achieved.

If goals aren’t met, businesses can still better understand what needs to be changed in the operating budget for the next period.

How it works…

Operating budgets predict the company’s income for the next few months to a year, so they can be created monthly or quarterly. Luckily, creating one is relatively simple and only requires your monthly sales, operating expenses, and labor costs.

Every month or quarter, take time to review your business budget to see where you’re standing. You should look to see if you’re overspending, underspending, or meeting your goals and answer whether or not your finances for a particular period are what you expected.

Type #2: Financial budget

Along with the operating budget, financial budgets are the other essential aspect of your master budget.

The goal of your financial budget is to present your company’s strategy for managing assets, cash flow, income, and expenses so that business and finance leaders can accurately see where, why, and how the company is spending and making money.

Who it’s for…

Financial budgets essentially weigh the value of your company because they measure:

- Cash balance

- Capital expenditures

- Assets

- Liabilities

- Investments

While any company can use financial budgets, larger businesses focus more on them for decision-making and planning. This is because small organizations typically plan one to two years in advance, while enterprise organizations might plan a decade in advance.

Still, creating a financial budget is beneficial for small to medium-sized companies because it’s necessary for gaining valuable insight into your spending relative to revenues from core operations.

How it works…

The financial budget is where you get a clear view of what financial resources you have and where your money is going because it includes the budgeted balance sheet and cash flows.

When creating the financial budget, you’ll look at your plans for managing your assets, cash flow, income, and expenses. This essential type of budget requires plugging in real and forecasted numbers, which are used throughout the accounting period to ensure that everything stays on track.

Type #3: Cash budget

A cash budget is a company’s cash flow estimation over a specified period. This type of budget aims to help a business manage and measure its income (cash inflow) vs. expenses (cash outflow).

It’s important to know that we’re not just talking about all types of income and expenses in this instance: Cash flow reflects the business’s day-to-day operations. On the other hand, profits, for example, are an overview of the company’s ability to make more money than it spends.

Who it’s for…

Anybody can use a cash budget because it helps business leaders regulate their expenses and estimate whether they have enough cash to pay for their regular operations.

Cash budgets can also provide important insight into whether you’re overspending or underspending in certain areas so you can make adjustments and hopefully become profitable and more successful in the future. It’s also an essential way to help track seasonal changes and trends!

How it works…

Business leaders and managers use cash budgets to ensure that there’s enough money for all of their expenses each month, quarter, or year.

For example, say that your employees get paid every two weeks. Your cash budget lets you see whether you have enough cash balance between the payroll expenses that occur twice a month.

Type #4: Direct labor budget

A direct labor budget calculates the number of actual labor hours needed to produce units. It helps measure what it will cost to meet a production or service goal so you can accurately balance the working hours vs. payroll expenses without going over budget.

A labor budget also affects your employee schedule and shifts. You can use it to ensure you’re not over-scheduling or under-scheduling.

Who it’s for…

A labor budget is an essential aspect of your business budget no matter what industry you’re in, especially since labor can make up 70% of your costs.

As an example, a bakery will need to use a direct labor budget to ensure it has enough money to pay employees to bake the bread on a given day.

How it works…

Businesses usually create a monthly or quarterly labor budget since it’s essential to keep a close eye on employee costs. You can calculate your budget by gathering the number of units needed and multiplying that number by the standard labor hours for each unit.

This calculation will give you a subtotal of direct labor hours required to meet your target.

Say that your bakery needs 25 loaves of bread baked fresh every day, and each loaf requires an hour of prepping and baking. You’ll multiply 25 loaves by one hour, which equals 25 total labor hours.

You may decide to have five employees in the store each morning so that they can spend five hours baking to meet this 25-loaf target.

Type #5: Static budget

A static budget is one of the most straightforward and most-frequently-used budgeting formats because it’s used as a basis to compare to actual results. A static budget does not change no matter what the company’s activity levels are.

It anticipates a fixed amount in sales, revenue, and expenses throughout a specified accounting period.

Who it’s for…

A static budget is typically used to keep track of ordinary expenses like rent, insurance, payroll, and utility costs, which are essential for keeping track of your fixed expenses.

They’re ideal for beginning budgeters since they’re easy to implement, don’t require consistent updating, and of course, provide helpful insight into the company’s expenses.

But static budgets are also great for businesses with very predictable sales and expenses, like utility companies.

How it works…

A static budget essentially predicts a business’s variable and fixed costs, which means that you’ll be tracking actual output, volume, and revenue throughout the accounting period.

Say that a growing small business has a projected sales number of $500,000 and decides that its sales commissions are fixed at $10,000. If the actual sales are only $400,000, then the sales commissions are still $10,000.

It’s helpful to have these baseline figures when making business decisions.

Type #6: Capital Budgets

A capital budget can help a business plan for larger investments or purchases of large assets, including vehicles, machinery, property, and more. Ideally, these purchase or investment opportunities would be evaluated ahead of time and identified based on their potential to generate returns over time.

Who it’s for…

Businesses looking to make sizable investment in equipment or property in the future may want to consider implementing a capital budget. This can help the business know exactly how much to allocate to the purchase, and where external funds or financing may be necessary.

How it works…

Once an opportunity is selected, funds are directed to the acquisition of the asset. This can involve cash or internal funds, or possibly external financing.

The process of creating a capital budget and then securing assets should also include a plan to monitor the progress of each acquisition and to document appreciation or depreciation and other factors.

Type #7: Overhead Budgets

An overhead budget includes both variable and fixed overhead expenses for a designated period of time. These expenses are associated with the ongoing operations and support functions of the business.

Who it’s for…

Any business looking to get a better understanding or greater control of their overhead costs can benefit from an overhead budget. Creating and regularly revising an overhead budget can help business owners understand where funds are going, where they can scale back or reallocate, and opportunities for growth or savings.

How it works…

An overhead budget can include the following:

- Administrative expenses

- Marketing and advertising expenses

- IT expenses

- Research and Development (R&D) expenses

- Facilities and maintenance expenses

- General or miscellaneous expenses

Exploring the types of budgeting systems

Now that you’re familiar with the most common business budgets, finding the right budgeting approach is key to a successful plan. Here are some budgeting systems you should know when deciding how you want to organize your budget.

Type #1: Traditional budgeting

As its name denotes, traditional budgeting is the oldest and most common budgeting method for businesses worldwide. It follows one simple rule: This year’s business budget is based on last year’s spending.

There is no set formula for traditional budgeting since business leaders have to use the previous year’s expenditures as a starting point.

Since this method follows each year’s spending habits, it’s easy to spot issues and make appropriate changes. This can be especially helpful if a business plans to apply for financing or expand its operations sometime down the line.

If a company sees that it can have the potential to double in size, then it may apply for a loan. Business leaders will share concrete financial and operating projections when applying for the loan, which makes it easier to get approved.

Type #2: Zero-based budgeting

Zero-based budgeting is a simple budgeting method that allows your business to start from zero and build up based on your average expenses. This method allows all department budgets to start at zero and is adjusted according to project costs and other expenses.

It’s an excellent method for those who like to start from scratch with a clean slate.

Zero-based budgeting increases efficiency, accuracy, and communication within the sales department. This method can directly involve employees in decision-making. This is critical, as their input can help managers cut unnecessary costs.

Business leaders have the opportunity to directly involve employees in sales, operations, manufacturing, and finance departments who have a unique perspective that can highlight blind spots that managers might otherwise miss.

Type #3: Rolling budgeting

Rolling budgeting is a unique method that focuses on short-term goals rather than long-term, which means that managers should update these budgets monthly to maintain control over revenue vs. expenses. These continuous budgets help managers understand how the company is doing in sales and profitability.

Rolling budgeting is all about continuing the budgeting cycle. When one accounting period ends, all you have to do is add the following month instead of starting a new budget from scratch.

Businesses that require this type of flexibility involve fast-paced, unpredictable environments where trends and patterns are ever-changing, like real estate, retail, and consumer goods.

Say that a small business that specializes in curating gold jewelry has found that buyers are more interested in silver jewelry. That business will use a rolling budget to adjust the cost and quantity of their material expenses, which will hopefully positively impact their total revenue.

Type #4: Flexible budgeting

Unlike a static budget, a flexible budget adjusts based on changes in revenue, expenses, and other business-related activities. It ultimately helps managers gauge actual changes and costs in real-time, whereas static budgets remain unchanged.

Since flexible budgeting changes based on activity levels, this method also is helpful when measuring a manager’s efficiency.

Take a look back at the static budgets example. With a flexible budget, business leaders will instead adjust the sales commissions based on the lower income by a set percentage.

If the business decides to reduce the sales commissions by 5% for every $100,000 lost, the sales team would only receive $9,500.

Choosing which types of business budgets and budgeting methods to use can take some trial and error. But, as you optimize your budgeting processes, you’ll gain invaluable insights that can be used to enhance business performance and growth.

Start making smarter business decisions with the right tools

Even though complexity levels vary depending on your type and size of business, budgeting activities are essential for making financial and business decisions that are rooted in data.

Using business budgets to inform your decision-making will pay off in the long term as good choices will help you attract potential investors, get approved for loans, and of course, create a more loyal customer base.

But keeping track of your finances is no easy task, which is why thousands of businesses rely on a software solution that helps track expenses, revenue, and profit, all while ensuring better business modeling and accurate forecasting.