Today's world involves businesses making transactions across nations and continents. What keeps it all going?

In order to help facilitate international financial transactions across different countries each day, a number of financial institutions connect to one another, creating an international banking network.

One institution in this network is the intermediary bank, a vital organization that directly helps banks in different countries transfer funds quickly and securely from one to the other.

What are intermediary banks?

Before defining what an intermediary bank is used for, let's also identify the other financial institutions it interacts with. These include:

- The sender bank

- The receiving bank

Whenever international wire transfers occur, an intermediary bank acts on behalf of the sender bank — also called the originating bank — to send payments to the receiving bank, which is also called the beneficiary bank. The individual or business parties involved use the sender's bank to make payments through their local bank account. This is also referred to as the originator bank because it is where the person or business will transfer money to the receiving bank.

An individual or business entity uses the receiving bank to collect payment in their bank account and is the final destination of payments from the sender's bank. Receiving banks are also called beneficiary banks because the beneficiary receives money from the sender.

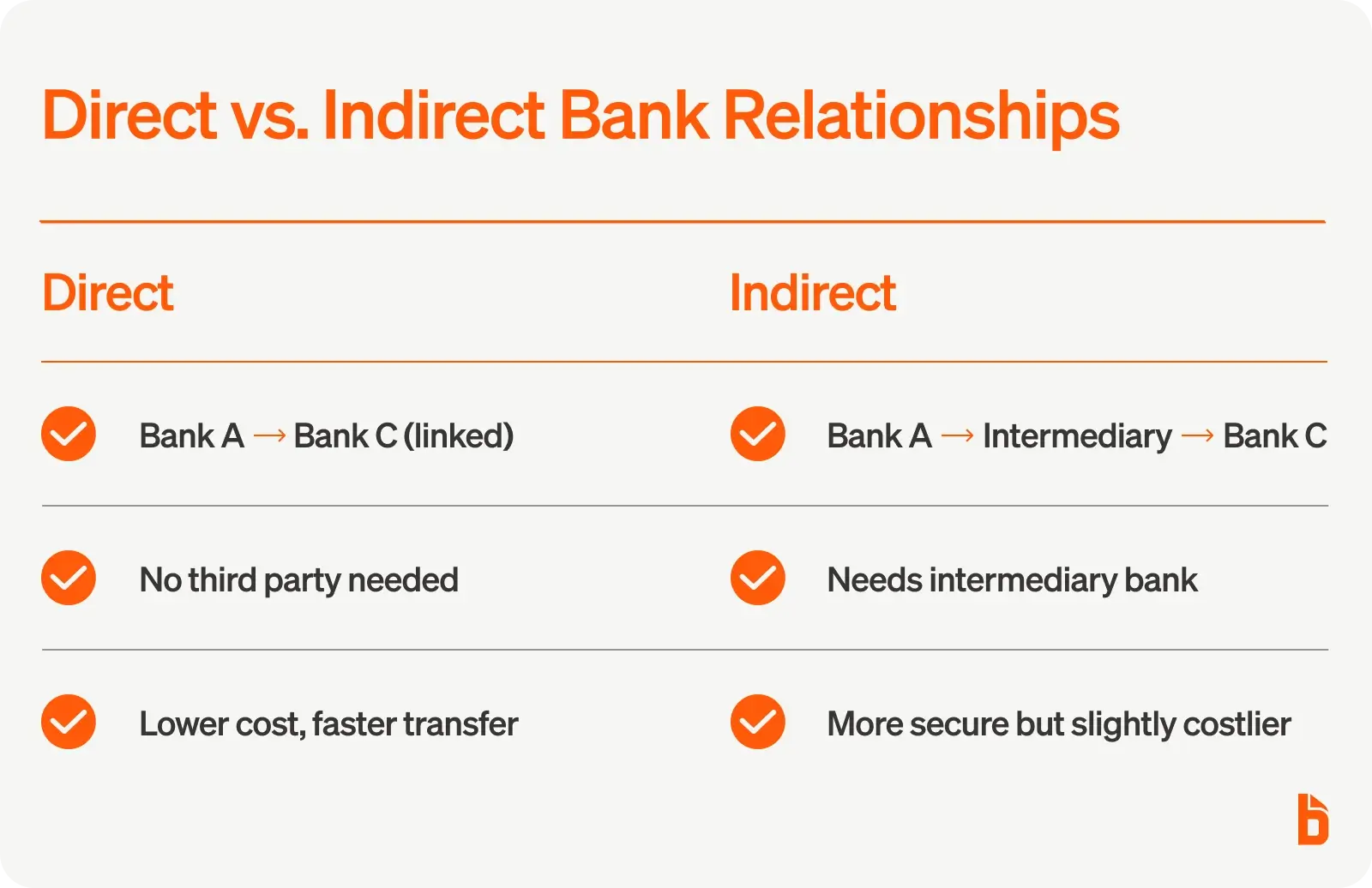

Finally, because the two banks are often located in different countries and don't have a direct relationship, an intermediary bank is used to create a more well-established relationship. This whole process helps the originator's bank send payments quickly and ensures the beneficiary bank receives them more securely, creating a safe and stable network for international transfers.

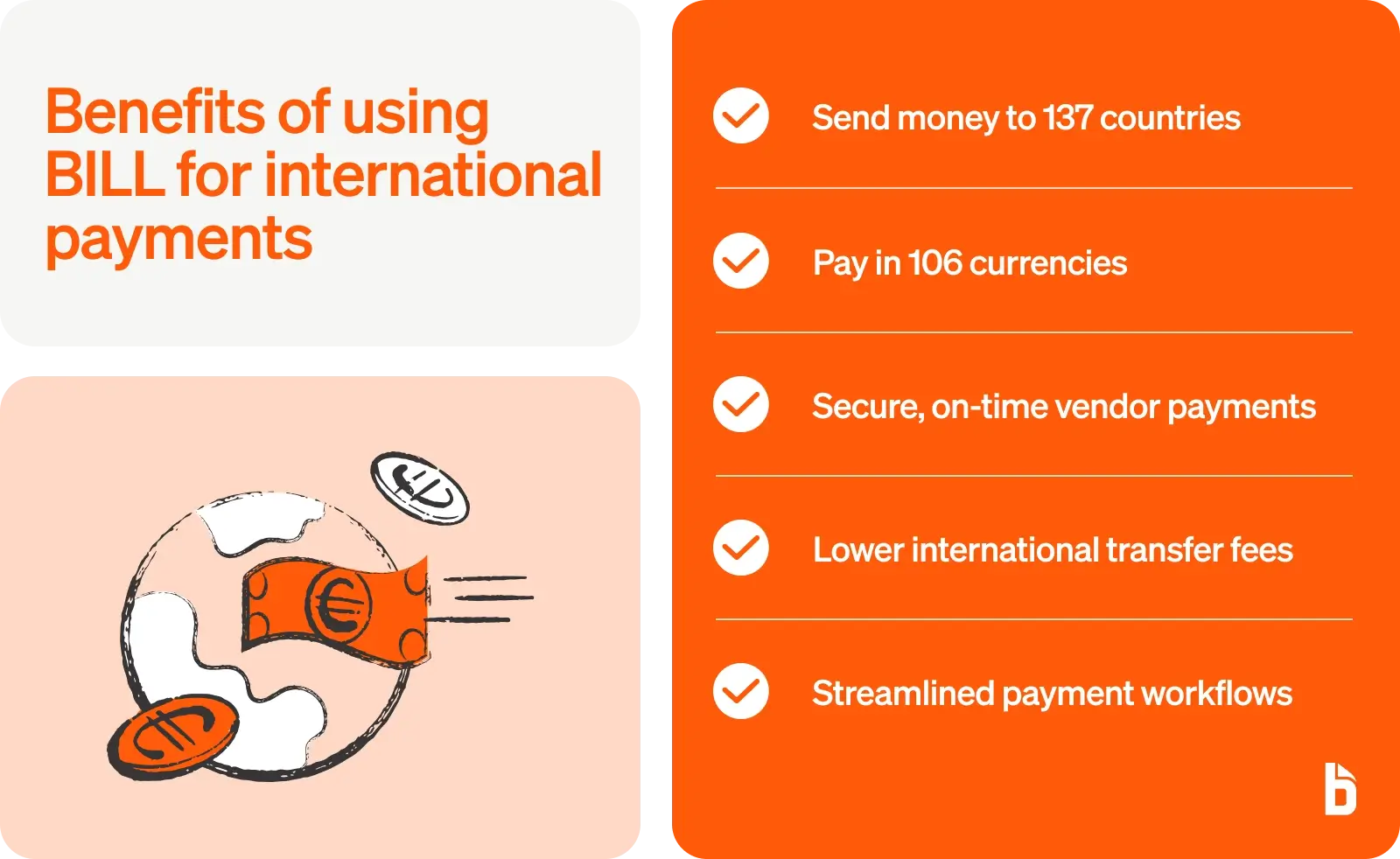

Simplify international transfer payments even further between a domestic bank and a foreign recipient's bank with BILL's international payment platform. Streamline workflows and save your business money from standard fees.

What is an example of an intermediary bank?

The function of an intermediary bank in an international transfer payment looks complicated but is relatively simple. Here's an example of how intermediary banks can help companies with paying suppliers:

- Tom owns an electronics retailer in France, while Kayleigh operates an electronics manufacturer in Belgium. Tom's company owes a payment to Kayleigh's company for several products they ordered.

- Bank A, where Tom holds his business bank account, has no banking relationship with Kayleigh's bank, Bank C. However, Bank B is an intermediary bank with connections to both Bank A and Bank C, allowing Tom to make international payments from his bank to Kayleigh's through the relationship they share through Bank B.

Although intermediary banks are known as third-party banks, making them seem less prominent, some of the world's largest banks, like CitiBank, HSBC, and JPMorgan Chase, are all intermediary banks that enable cross-border transactions.

How do intermediary banks work with other financial institutions?

Intermediary banks can work so effectively with every other financial institution largely due to the Society of Worldwide Interbank Financial Telecommunications, or the SWIFT network for short.

SWIFT is a payment network that allows banks to send and receive electronic money transfers worldwide.

It includes thousands of financial institutions playing different roles within the network, from originator and correspondent banks to intermediary and beneficiary banks. Generally, intermediary banks are members of the SWIFT network, supporting other member banks with every cross-border transaction they perform.For example, if two banks have a direct relationship both banks have accounts with each other and can easily send and receive money to their accounts. If two banks have an indirect relationship an intermediary bank is required because the two banks don’t have accounts with each other and will need a third party to assist with transferring the payments.

In addition to them, correspondent banks are another financial institution that also assists in international transfers and payments, performing a similar function to intermediary banks, but with a few key differences.

What's the difference between intermediary and correspondent banks?

Correspondent banks and intermediary banks are both third-party banks that help process international financial transactions. However, there is one key difference between the two that individuals and businesses should be aware of.

Firstly, correspondent banks often perform transactions with multiple currencies, while intermediary banks typically work with only one currency. Working with only one currency gives correspondent banks the advantage of being able to provide transactions that include currency exchange.

For example, if an individual transfers a payment from the U.S. to another person in Australia, the correspondent bank processes the transaction from the U.S. dollar into Australian dollars. This allows the recipient's bank to receive the correct amount without needing to exchange the currency themselves.

Take your small business international with BILL. Our streamlined payments system supports 137 countries and 106 currencies and improves international wire transfers to vendors and suppliers worldwide.

Are there intermediary bank fees to pay?

In addition to the litany of fees attached to international wire transfers, an intermediary bank charges several fees. Their fees, however, aren't standard, making it difficult to know how much they will add to the cost of an international wire transfer.

The total intermediary bank fee depends on the currency as well as additional fixed charges levied on each specific transaction. Furthermore, some international payments may require more than one intermediary bank, with additional fees that will increase the total balance before reaching the receiving bank.

How are these fees paid?

There are a few ways to cover intermediary fees and the additional transaction fees for wire transfers to different countries. Each one is settled between the sender and recipient before beginning the transaction. Here are three options based on the standard SWIFT form for international wire transaction costs:

Beneficiary (BEN)

This option involves having the beneficiary receive the entire amount of charges for the transaction, bearing full responsibility to pay fees from the intermediary banks and originator bank charges. This is often done by subtracting the total amount of fees from the wire transfer, leaving it so that the beneficiary receives less than the original amount from the sender's bank.

Originator (OUR)

In this case, the sender or originator pays for all fees from the intermediary bank and receiving banks. One difference to note here is that they receive a fixed fee upfront since the actual total fee cost of the transaction can only be calculated once the wire transfer is completed. This results in transactions where the receiver gets the precise amount they had charged, squaring everything away all at once — an ideal agreement for those seeking to pay their suppliers.

Shared (SHA)

Finally, this choice divides the total costs between the sender and receiver. The senders' fee will be a single standard, while the receivers pay for fees charged by their receiving banks as well as any intermediary fees. This option is very commonly used, as it nearly provides an even split among costs between both, leaving sender and receiver with the fairest possible results.

Make international payments a breeze with BILL

What is an intermediary bank used for? It's used to help businesses send payments or receive payments between two unaffiliated banks and helps companies big and small do business on a global scale.

On top of that, BILL's international payments system will streamline your workflow and get payments to your vendors on time while avoiding costly bank fees. Reach new heights for your business with BILL today!