What exactly are prepaid expenses?

Chances are, you’re already using them.

If you’ve signed up for an annual software subscription, paid a few month’s worth of your business's building lease in advance, or bought office supplies in advance, you’ve prepaid some expenses.

But are you recording these purchases as prepaid expenses in your financial accounts? Did you even know that was a thing?

In this article, we’re going to explain prepaid expenses.

We’ll explain what prepaid expenses are, how they are recorded in financial statements, common examples of prepaid expenses, and why its important for small businesses owners to be on top of them.

What are prepaid expenses?

Prepaid expenses are payments made in advance for goods or services a business will receive in the future. Common examples include prepaid rent, prepaid insurance, or subscriptions paid upfront.

In accounting, prepaid expenses are initially recorded as assets on the balance sheet because the payment has been made, but the benefit has not yet been realized. Over time, as the service or benefit is consumed, the asset is reduced and the expense is recognized on the income statement.

Is a prepaid expense a current asset?

Yes, prepaid expenses are typically considered a current asset on a company’s balance sheet.

That’s because prepaid expenses are generally expected to be consumed within the next 12 months.

If you’ve paid prepaid expenses even further in advance — such as a three-year software contract — your accountant may record this as a non-current asset, though this is less common.

How are prepaid expenses recorded in financial statements?

Recording prepaid expenses properly is an easy two step process. But before you start recording the transactions on your books, you need to know whether you can based on your accounting method.

Prepaid expenses in accrual vs cash basis accounting

There are two main methods of accounting: accrual and cash basis.

With cash basis accounting, you only record transactions when cash changes hand. Because of this, prepaid expenses don’t exist on financial statements with the cash basis method.

If you prepay an expense, you must record the entirety of the payment when it happens. For example, if you paid for an annual insurance policy upfront, you must record the entire amount when payment is made rather than amortize it over twelve months.

With the accrual method, transactions are recorded twice: when the good or service is provided and when the payment is made.

If you use the accrual method, then you can record prepaid expenses in these two steps.

Recording the initial payment

Prepaid expenses are initially recorded in financial statements as current assets.

The expenses paid for in advance will then be listed under current assets on the balance sheet. Since the prepaid expense account is an asset, debiting it increases the balance.

As the prepaid expense is used up, it must be recognized in the income statement under the relevant expense category.

Recording the expense in an accounting period

The value of a prepaid asset is expensed over time on the income statement. As the expenses are actually incurred, invoices are received for the goods or services, and the benefits of the purchase are realized, journal entries are created.

As an example, say you paid a year’s worth of insurance premiums upfront.

Every month, you would record the above journal entry for 1/12th of the paid amount. Each journal entry reflects that one month of value is being realized by the business.

Follow these steps on a regular basis, and you’ll ensure your financial reporting is accurate and up-to-date.

Common examples of prepaid expenses in accounting

Any expense paid for in advance can be considered and recorded as a prepaid expense.

These are some of the most common examples you’ll come across in financial statements:

- Insurance premiums. These are very commonly paid on an annual basis.

- Software subscriptions. Most software is purchased on a subscription basis. Businesses can take advantage of better pricing by paying quarterly or annually, which can be considered a prepaid expense.

- Rent and leases. Organizations often pay the rent on their factory or office space in advance and do the same for leasing equipment, machinery, and vehicles.

- Utilities and telecommunications. Some utility companies may require advance payment.

- Maintenance agreements. Ongoing maintenance and cleaning contracts may be paid in advance annually or quarterly, even though they are only realized monthly.

- Retainers. Sometimes marketing, advertising, and legal retainers are offered with discounted pricing for advance, which can be reflected as prepaid expenses in financial statements.

- Taxes. Certain taxes, such as property taxes, may be paid in advance. Some tax bodies require provisional tax to be paid in advance, which could also be considered a prepaid expense.

Why do small business owners need to understand prepaid expenses?

Many small business owners are already paying for certain expenses in advance, but they may not be properly accounting for them in their financial statements.

Here’s why it's important to get a better handle on prepaid expenses and how they are used.

Impact on cash flow

Prepaid expenses mean an immediate cash outflow, even though you’re not going to be realizing the benefits of the goods or services you’re paying for some months to come.

This can strain cash flow if not planned properly.

Equally important here is planning for future prepaid expenses. If you’ve paid for a large software bill on an annual basis right now, you’ll still need to put money aside to ensure you can meet that recurring expense 12 months from now.

Impact on financial statement accuracy

Recognizing prepaid expenses in your financial statements is critical.

Any expense that is considered prepaid must be recorded as a current asset on the balance sheet and then gradually expensed over the period to which they relate.

Doing so ensures that your financial statements reflect your company’s true financial situation, something current and potential investors will want to confirm is the case.

It also helps you align with the matching principle.

This is an accounting principle that states that expenses should be recorded in the same accounting period as the revenues they help to generate, as opposed to when the actual cash is paid out.

Misclassifying prepaid expenses as immediate costs can lead to understating your business's assets and overstating your outgoings, which can skew financial reports and negatively impact business decision-making.

How prepaid expenses affect your taxes

Prepaid expenses don’t just affect your financial statements, they can impact the amount you pay in taxes.

It’s commonly suggested to prepay expenses towards the end of the tax year to rack up tax deductions and save money on your tax bill. But generally speaking, prepaid expenses must be amortized over the period of usefulness.

The IRS has what’s called the 12-Month Rule for determining when you can report your prepaid expense.

Under the 12-month rule, the entirety of the prepaid expense can be reported in the current tax year if it meets the following conditions:

- The benefits do not extend beyond 12 months after the agreement begins

- The benefits do not extend beyond the end of the tax year after the current tax year in which the payment is made

To illustrate this, say you prepay a year of rent on July 1st. Since a year of rent does not provide value beyond 12 months nor provides benefit beyond next tax year, it meets the 12-month rule condition.

But if it was a prepayment for two years of rent, it would not pass the 12-month rule and must be spread out over the useful period.

Businesses have flexibility on when they report prepaid expenses under the 12-month rule. Do you want the tax benefit in the current tax year or spread out into next tax year? What you decide determines whether you report the entire prepaid expense on your taxes, or spread it out.

Keep in mind that this is for tax purposes only. Per the Generally Accepted Accounting Principles (GAAP), prepaid expenses must be spread out on your financial reports, regardless of how you will be reporting the expense for tax purposes.

Strategies for managing prepaid expenses

Now that you’ve got a good idea of what prepaid expenses actually are, let’s cover off a few best practices for managing them.

Use financial management software

Using financial operations software is a good practice in general, but doing so can help you automatically map prepaid expenses over to the income statement as they are actually realized, ensuring you align with the matching principle.

Create a prepaid expense schedule

Use your financial management software tool to create and maintain a detailed schedule of all prepaid expenses, including conversion timelines, so you have an easily accessible report to access when conducting audits.

Conduct regular audits

Implement an auditing cadence — quarterly should work for most businesses — where you review:

- All new prepaid expenses incurred for the period to ensure they have been recorded accurately.

- All existing prepaid expenses recorded to ensure that they are being expensed correctly on the income statement.

Prepaid expenses vs. accrued expenses

Prepaid expenses and accrued expenses are two kinds of entries you’ll find on financial statements.

They both relate to how a company records its expenses but represent opposite scenarios.

Prepaid expenses are those you’ve paid in advance for several months or even up to a year. They are recorded as a current asset and gradually expensed onto the income statement as they are recognized across the financial period to which they relate.

Accrued expenses are the opposite. They are recognized and have been incurred during the current financial period but have not yet been paid

They are recorded on the balance sheet as current liabilities. That liability is then reduced when a payment has been made, and cash comes out of the bank account.

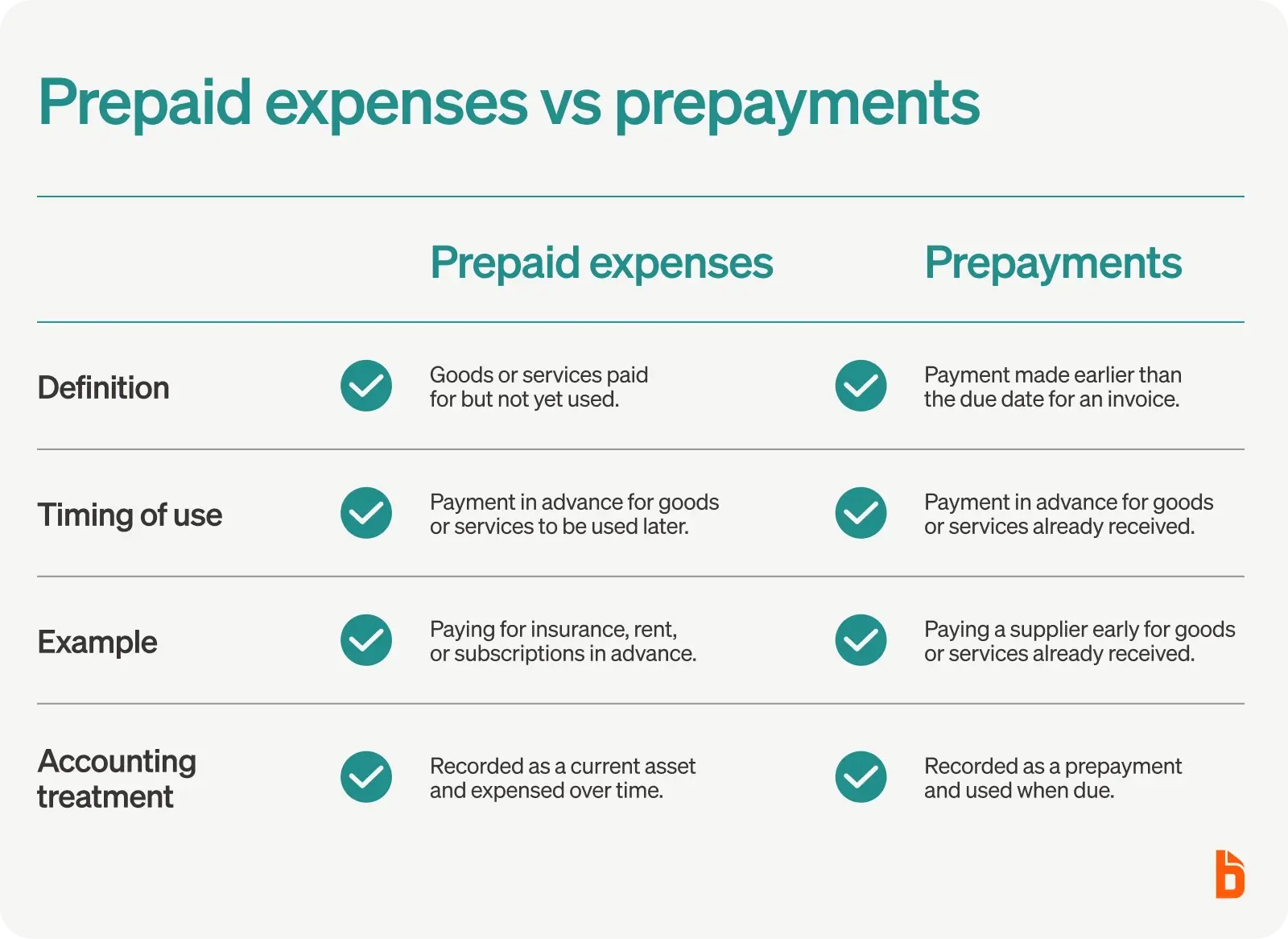

Prepaid expenses vs. prepayments

Prepaid expenses and prepayments sound similar, but they are not the same thing.

A prepayment just means you pay your invoice earlier than the due date. For example, if you have a payment to a supplier due next month, but you decide to pay it now, that’s a prepayment.

A prepaid expense is a good or service you’ve paid for but not yet used.

That’s the key difference. Prepayments are for goods or services received and used but for which the invoice is not yet due.

Get on top of prepaid expenses

Prepaid expenses are an important part of financial recordkeeping.

Any time you pay for business expenses in advance of receiving and using them, you’re incurring prepaid expenses, and this needs to be reflected correctly on your financial statements.

The most effective small business owners keep on top of business expenditures — including prepaid expenses — with a modern, intelligent expense management solution.

These software platforms, such as BILL, can help you manage spending with employee spend cards, deep reporting capabilities, and insightful forecasts.

Dive into BILL Spend & Expense today and take control of prepaid expenses.