Accounting principles are like the building blocks of a successful business: They set the foundation for understanding your company’s financial performance so you can create the right trajectory for growth.

Adhering to these principles also makes it easier for all stakeholders to have a full-fledged picture of your company’s financial health. But what exactly are accounting principles—and how can you use them to benefit your business?

The ins and outs of accounting principles

Accounting principles are the basic rules and standards businesses must follow when reporting their financial data to stakeholders, the public, and the IRS.

Initially, they were established to improve the quality of financial reporting across industries while ensuring that all companies provide their financial transactions and report the same way.

Because using accounting principles increases transparency in financial reporting, companies can see red flags quickly and respond accordingly. This helps mitigate fraud while maintaining reputation and credibility.

And if you’re wondering why accounting principles matter, the answer is simple—they matter because they ensure that investors, auditors, and shareholders can compare financial statements coming from different companies with ease.

Thanks to accounting principles, a financial statement doubles as a powerful comparison tool that external stakeholders can use to make economic or investment decisions.

Down the accounting memory lane

While the history of accounting goes back thousands of years, the federal government developed most of today’s accounting standards and rules to respond to the Stock Market Crash in 1929 and the challenges of the Great Depression period.

Before the 1929 crash, some public companies used less-than-honest reporting practices. Inaccurate financial tracking led to a lack of transparency, helping trigger these historical events since investors didn’t have the information they needed to make rational decisions.

The post-Depression era marked a turning point in how the Financial Accounting Standards Board (FASB) established accounting rules and practices, including the well-known generally accepted accounting principles most U.S.-based businesses use today.

With new reporting expectations, like the disclosure principle, the way companies report their financial statements changed forever. And it was all in the name of ensuring financial completeness, consistency, and comparability across all industries so a lack of transparency wouldn’t harm the economy again.

Who sets accounting principles and standards?

A few financial governing bodies ensure accounting standards are upheld as they should be.

For starters, accountants for American businesses follow the rules created by the Financial Accounting Standards Board (FASB), which has set the financial accounting standards in the U.S. since 1973.

FASB uses generally accepted accounting principles (GAAP) as the foundation for its comprehensive set of approved accounting methods and guidelines. Other existing measures include the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB).

But one thing to keep in mind is that there is no global set of accounting standards. If you are a U.S.-based company, you follow the generally accepted accounting principles. If you are an international copy or have foreign subsidiaries, you follow the International Financial Reporting Standards.

Although FASB and IASB have different accounting principles, they sometimes cooperate, such as when there is a need to establish new joint standards important to businesses.

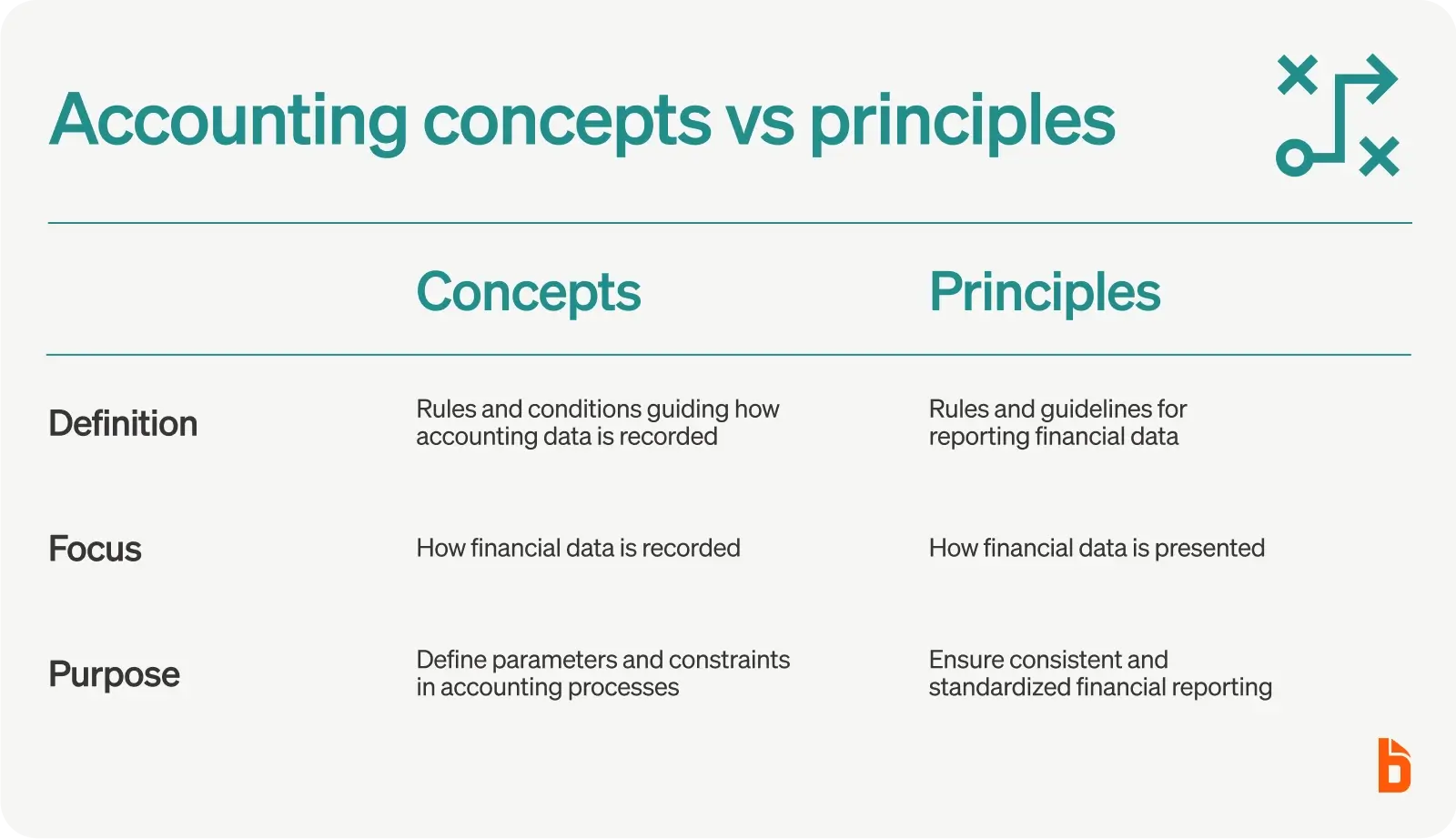

Accounting concepts vs. accounting principles

Before exploring the foundational accounting guidelines, let’s first understand the primary difference between accounting concepts and principles:

- Accounting concepts are important rules and conditions that define the parameters and constraints within the way accounting operates, which determine how accountants record accounting data

- Accounting principles put forward a set of rules and guidelines that companies and other entities must follow when reporting financial data

In simpler terms, accounting concepts represent the way you record financial data, while accounting principles determine how you present such data.

Fundamental accounting concepts

Whether you are a business owner who handles some of your company’s financial reporting or use an accountant to handle the bookkeeping, it’s still essential to understand how you should record financial data.

Here is a list of the fundamental accounting concepts any business owner should know about:

Economic entity concept

Based on the economic entity concept, you should keep all transactions separate because a business and its owner are separate individual entities. The statute recognizes the entity as an artificial person. In doing so, the company’s financial statements will never mix personal finances with business transactions.

Going concern concept

All financial statements should be prepared assuming the business will not cease to exist in the foreseeable future. The assumption is that there will be another accounting period.

And with this assumption in mind, revenue and expenses can be recognized at a later, future period. If the company won’t still be operating, expense recognition comes in the current fiscal period.

Materiality concept

In tandem with the disclosure principle, the materiality concept notes that all significant transactions and notes that hold decision-making value should be part of financial statements.

For example, if your company has a situation that would change someone’s mind about investing in your company—like influencing a business decision—it should be recorded in the corresponding financial statement.

Industry practices constraint

Since some industries have unique business operations, they do not need to conform to traditional accounting principles.

The agriculture industry is an excellent example of this: Crops are reported at the market value on the balance sheet instead of the conventional route of using historical or production costs.

Since calculating the actual cost per crop can quickly become costly and complicated, this industry can modify its accounting practices to what works best for them while still maintaining transparent and accurate financial reports.

Basic accounting principles

The following accounting principles make up today’s financial reporting standards.

These principles apply to every accounting standard and are fundamental because they serve as the foundation for GAAP and IFRS (with the former applying to U.S. companies only and the latter applicable internationally).

Let’s take a closer look at what the basic accounting principles entail.

1. The revenue recognition principle

The revenue recognition principle—a feature under accrual accounting—requires revenue to be recognized when earned, which provides a more accurate financial picture. In other words, your company does not need to wait for cash from customers to record the revenue coming from sales.

Let’s put the revenue recognition principle into practice: If your repair company hires a contractor to fix the roof for a customer, and the job is completed, you have earned the revenue from that job. This happens whether or not the customer has paid you.

The new ASC 606 revenue recognition model

Recently, the FASB and IASB teamed up to develop ASC 606.

ASC 606 provides a framework for all businesses—public and private—to recognize revenue the same way to:

- Help create concrete contracts between businesses and customers

- Establish proper quotes and pricing in those contracts

- Correctly identify when revenue is fulfilled from these contracts

- Ultimately prevent fraud, non-payment, and misunderstandings between customers, companies, and stakeholders

Although it’ll take years for all businesses to catch up with the new standard, ASC 606 has a 5 Step Model for Revenue Recognition that is easy to follow:

1. Identify the contract with the customer: When establishing a contract with a customer, the contract must be approved by all parties involved who all agree to perform their obligations.

Example: If a catering business, John’s Catering, is hired to cater a wedding, the contract would require the catering company to provide goods (food) and services (serving) and the customer to pay for those goods or services.

2. Identify the performance obligations in the contract: The contract should clearly state what obligations are expected from the company supplying the goods or services.

Example: John’s Catering’s obligations may include adhering to a certain menu delivered by a certain time and day.

3. Determine the transaction price: The total cost of the services must be decided.

Example: John’s Catering would quote the customer a total price for their services.

4. Allocate the transaction price: If a single good or service is being provided, then there is no need to allocate the transaction—but in many cases, there are several aspects to consider.

Example: John’s Catering may allocate the transaction price into categories, such as travel time, setup, serving, appetizers, courses, desserts, and cleanup.

5. Recognize revenue when or as the entity satisfies a performance obligation: This step ultimately determines when payment is due—should it be paid upfront, or can it be paid after the services are provided?

Example: John’s Catering may request a 25% security deposit upfront to book their services and then require the rest of the amount within a week before the event.

2. The matching principle

For tax purposes, many small businesses prefer to operate on a cash basis—which means they report revenue when cash is received. Expenses are also recorded when cash is spent or the company’s credit card is used.

With the matching principle, businesses must record the expenses with the revenue earned.

For example, say that your company pays a 10% commission to a sales representative at the end of each month, and your company has $80,000 in sales in December. In this case, the commission will be $8,000 for the upcoming January.

Other matching principle examples include wages, employee benefits, and depreciation.

3. The conservatism principle

Conservatism is looking at your estimates, accruals, and uncertain outcomes like lawsuits. Under the conservatism principle, you should tend toward recording the loss, even if there is uncertainty about incurring a loss. But if there is uncertainty about recording a gain, you should not record the gain.

Let’s take a company, XYZ Ltd., for example. XYZ Ltd. is suing ABC Ltd. for patent infringement—and the good news is that they’re expecting to win a substantial settlement. But since the settlement isn’t a guarantee, XYZ Ltd. doesn’t record the gain in the financial statements.

XYZ Ltd. doesn’t record this in their financial statements because they may or may not win the settlement. Since a sizable winning settlement amount may lead to complexities in financial statements and mislead users, this gain is not recorded in the books. And since ABC Ltd. may expect a loss, they should record this loss in the footnotes of their financial statements.

4. The principle of substance over form

Substance over form states that financial statements and facts disclosed to the public about a business should accurately reflect the true realities of each transaction. All recorded transactions shouldn’t hide their true intent, so they don’t mislead the readers of your company’s financial statements.

This principle exists because it argues that an accountant may deliberately hide the true intent of a transaction, whether it’s because the accountant is trying to mislead or is trying to simplify an over-complex transaction.

Here’s an example of this issue with two companies, A and B. Because Company A acts as an agent for Company B, it should only record sales for Company B in the amount of the commission. But Company A wants to make its sales appear bigger, reporting the entire sale amount as actual revenue.

5. The historical cost

The historical cost requires companies to accurately reflect the price of the purchased goods, services, or other assets. The balance sheet should reflect the actual price of the assets within the set accounting period without any adjustments to the market value of goods.

Let’s take another example of Company A.

Company A purchased land in 1971 for $20,000. While the information in the financial statements is accurate, and we know how much the company paid for this long-term asset, this information does not reflect the current value of the land. Regardless, the balance sheet must maintain this $20,000 amount until the company sells the land or something changes.

How these accounting principles benefit small business owners

By following these accounting principles, you can accurately track and record expenses. And with that, you can also provide accurate financial information to shareholders and investors, which ultimately helps them make informed decisions.

Of course, making informed decisions is just one of the benefits, so let’s explore some others:

Benefit #1: Establish consistency in financial statements

Using established accounting principles makes it easier for your company to have consistency across all essential financial statements (including income statements, cash flow statements, and balance sheets).

It also leads to transactions that demonstrate the actual financial state of your company. For example, if your company recognizes expenses later on some reports, it could lead to a higher net income than your actual income, impacting your business decisions accordingly.

Consistency across your financial statements ensures that investors can better understand your company’s financial performance than others.

Benefit #2: Ease of auditing financial statements

Businesses that utilize accounting principles are easier to audit because auditors know and apply them when comparing financial statements. It also simplifies the entire audit process because it increases the credibility of provided financial information.

Benefit #3: Mitigate fraud

With the help of established accounting principles, you and your stakeholders gain a layer of visibility into your business’s finances.

With the disclosure principle—an essential accounting principle that requires an entity to include all the financial statements that may influence the understanding of the financials—having accounting information presented clearly and consistently makes it easier to detect and prevent fraud.

In essence, it ensures your company has the needed financial protection.

Benefit #4: Flexibility

You can use accounting principles in different situations. For example, the matching principle can be used in any business, banking or healthcare, since all companies get revenue and incur expenditure. This makes it possible to apply accounting principles to unexpected transactions.

Critiques of accounting principles

Accounting principles do not come without their fair share of opposition: Some believe that these principles provide too much freedom to companies.

For example, one could argue that these principles let a company present an inaccurate picture of its financial health—and misrepresentation does not align well with the need for transparency among businesses.

Others hold that since only monetary items are recorded, other events that might be of great importance but are not measured in such terms remain unaccounted for.

But one thing is for sure: Without these basic accounting principles, companies would not have any set of standards to ensure continuous investment and profitability.

Eliminate accounting confusion with expense management software

Accounting principles make it easier to track financial performance and share information on your company’s financial health with stakeholders. Adhering to these principles means sticking to a consistent financial reporting format through proper tracking and recording of expenses.

The best part? Everything you need to know about your company’s financials—such as creating appropriate financial reports and adhering to federal regulations—is available through the highly-rated and easy-to-use expense management software from BILL Spend and Expense.